Software Development

Software Development

Security Services

Security Services

Cloud Services

Cloud Services

Other Services

Other Services

TechMagic Academy

TechMagic Academy

Mastering Omnichannel Banking Implementation: Best Practices and Strategies

Director of FinTech at TechMagic. Ex-VP of Goldman Sachs. Blockchain and Web3 expert. Experienced engineering manager and CTO.

In the digital era, how do banks and financial institutions ensure they keep up with customer expectations? To boost sales, banks must blend digital convenience with good old-fashioned human interaction to create a seamless omnichannel experience.

According to Capgemini, 76% of customers now expect an omnichannel experience, with 59% demanding on-demand, anytime customer service. It's not just about the convenience of mobile apps anymore; it's about crafting a seamless environment where customers can effortlessly transition between different channels. This expectation for seamless interactions transcends industries, and the banking sector is no exception.

Where customers are inundated with options and alternatives, providing a seamless customer experience isn't just a nice-to-have—it's a necessity. Customers today are empowered and discerning, and they won't hesitate to take their business elsewhere if they encounter friction or inconvenience.

That's where this guide comes in. So, if you're ready to learn how to implement omnichannel banking properly and position your organization for success in the digital age, let's dive in.

Omnichannel banking

The rise of digital technology has significantly influenced customer expectations in the banking sector. With the advent of online and mobile banking platforms, customers now expect seamless, convenient, and personalized experiences across all channels. They seek instant access to their accounts, quick resolution of queries and issues, and the ability to complete transactions efficiently from anywhere at any time.

Moreover, customers expect banks to leverage advanced technologies such as artificial intelligence, machine learning, and data analytics to anticipate their needs and provide tailored recommendations and services. In today's digital banking environment, customers value speed, security, and simplicity, driving banks to continuously innovate and enhance their omnichannel capabilities to meet these evolving expectations.

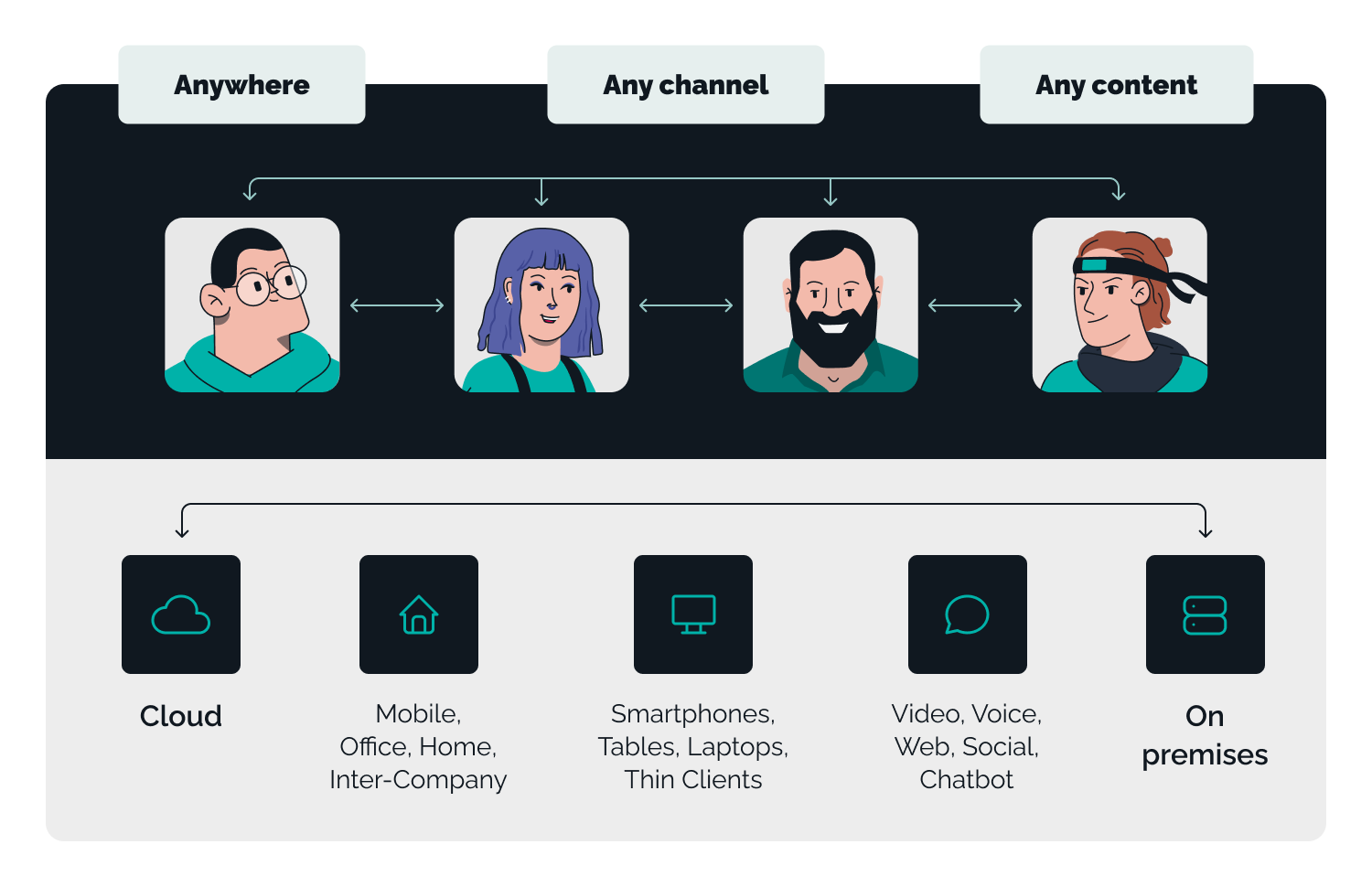

Omnichannel banking represents a holistic approach to customer engagement, where banks integrate multiple channels seamlessly to deliver a unified and consistent experience across all touchpoints. This requires a strategic alignment of various components to ensure a seamless customer journey, for customers, regardless of how they interact with the bank.

- Integrated Infrastructure: Omnichannel banking relies on a robust and integrated infrastructure that enables seamless communication and data sharing between different channels. This includes backend systems, databases, and APIs facilitating real-time access to customer information and transaction data.

- Unified Customer View: A central component of omnichannel banking is creating a unified view of the customer, consolidating data from various touchpoints to provide a comprehensive understanding of their preferences, behaviors, and transaction history.

- User Experience: Omnichannel banking aims to deliver a consistent user experience across all channels, ensuring that customers receive the same level of service and functionality regardless of the channel they choose to engage with.

- Cross-Channel Integration: Omnichannel banking involves seamless integration between different channels, enabling customers to transition effortlessly between online, mobile, and in-person customer interaction without encountering any friction or disruption. This includes omnichannel authentication, cross-channel transaction tracking, and synchronized account management.

- Personalization: Omnichannel banking leverages data analytics and machine learning algorithms to deliver personalized and contextually relevant experiences to customers.

Why omnichannel banking is the right choice

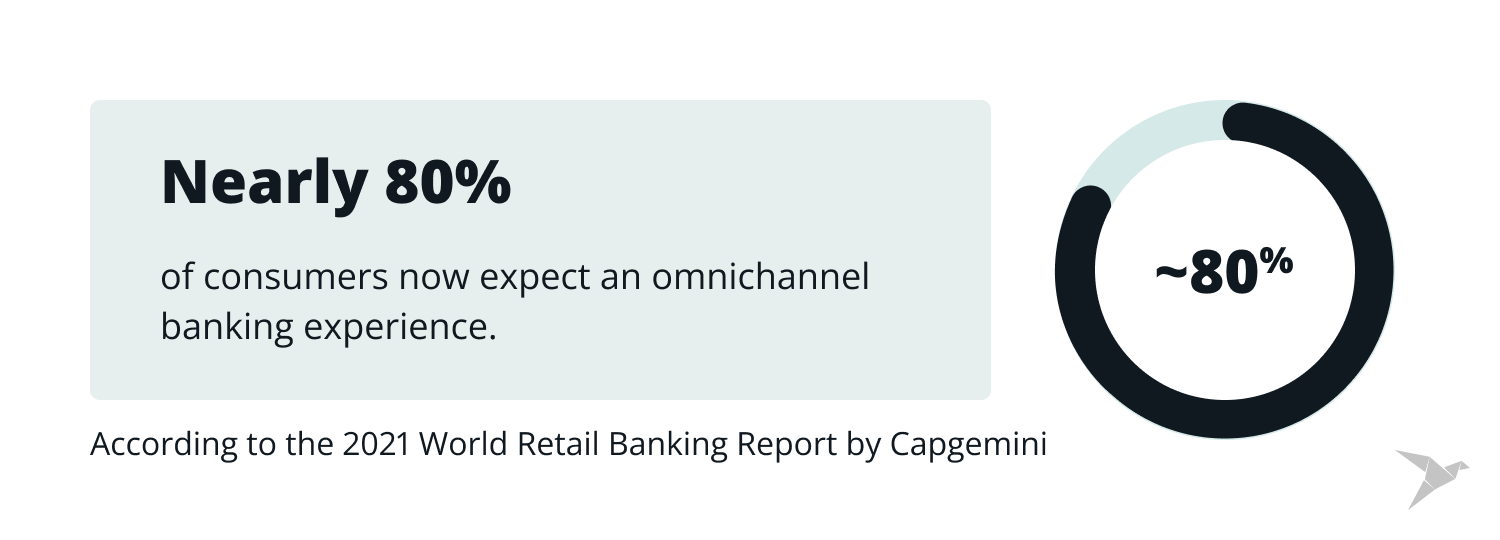

- According to the 2021 World Retail Banking Report by Capgemini, nearly 80% of consumers now expect an omnichannel banking experience. This statistic underscores customers' key role in driving banks to enhance their systems by offering more options for conducting banking activities. Consequently, there's a growing imperative for banks to prioritize omnichannel banking to meet these evolving expectations.

- The banking sector faces stiff competition from non-banking entities such as fintech companies, which provide comprehensive and user-friendly banking services through digital solutions. For instance, platforms like Chime offer mobile-first banking experiences, enabling customers to open accounts, make deposits, and conduct transactions seamlessly via mobile apps or online portals.

- Statistics from Statcounter reveal a significant preference for mobile and desktop platforms over physical visits for performing tasks. This trend underscores the omnichannel nature of modern interactions. In banking, customers increasingly opt for digital channels, reducing operational and maintenance costs for banks.

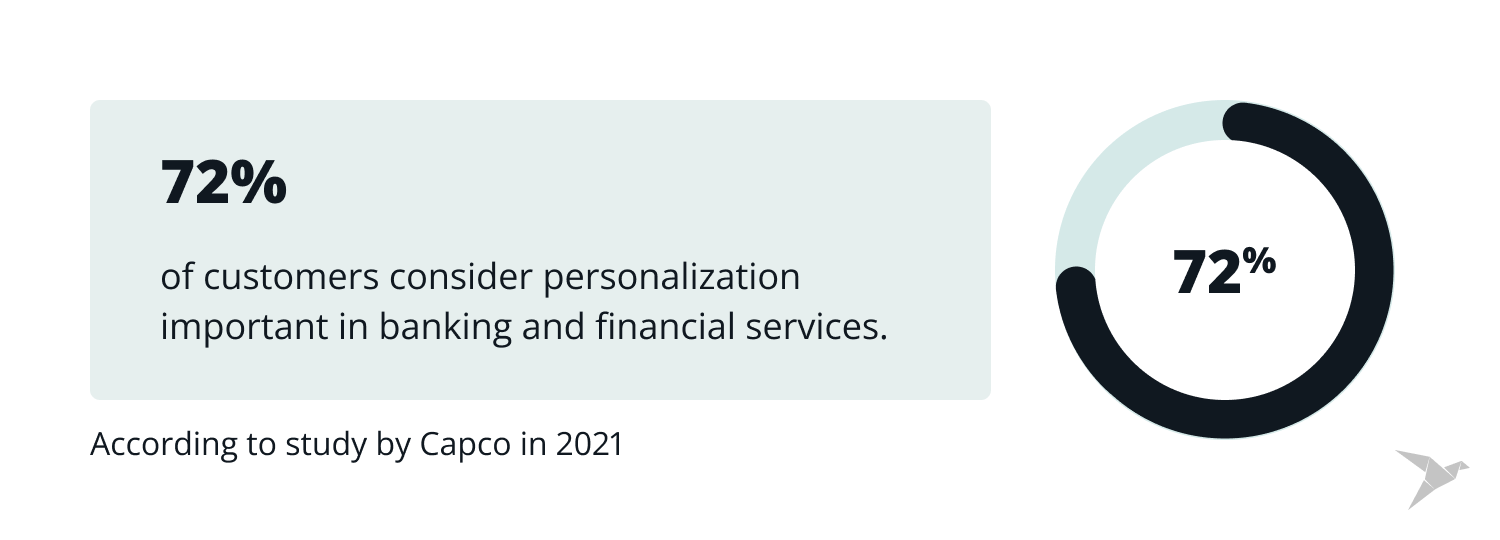

- A 2021 study by Capco found that 72% of customers consider personalization important in banking and financial services. As consumer expectations for personalized experiences continue to rise, banks face pressure to deliver omnichannel experiences that enable real-time interaction across all channels. This necessitates banks to invest in technologies that facilitate seamless synchronization and personalized engagement across various touchpoints to meet the evolving needs of customers.

- Omnichannel banking ensures that customers receive a consistent service experience across all channels, whether online, mobile, in-branch, or over the phone. Regardless of how customers interact with the bank, they can expect the same service quality, information accuracy, and support. This consistency fosters trust and loyalty among customers, as they feel confident knowing that their banking needs will be met seamlessly, regardless of the channel they use.

- With omnichannel banking, data management becomes centralized, allowing banks to access, analyze, and utilize customer data more effectively. By consolidating customer information from various touchpoints into a centralized database, banks can gain a holistic view of each customer's interactions, preferences, and behaviors.

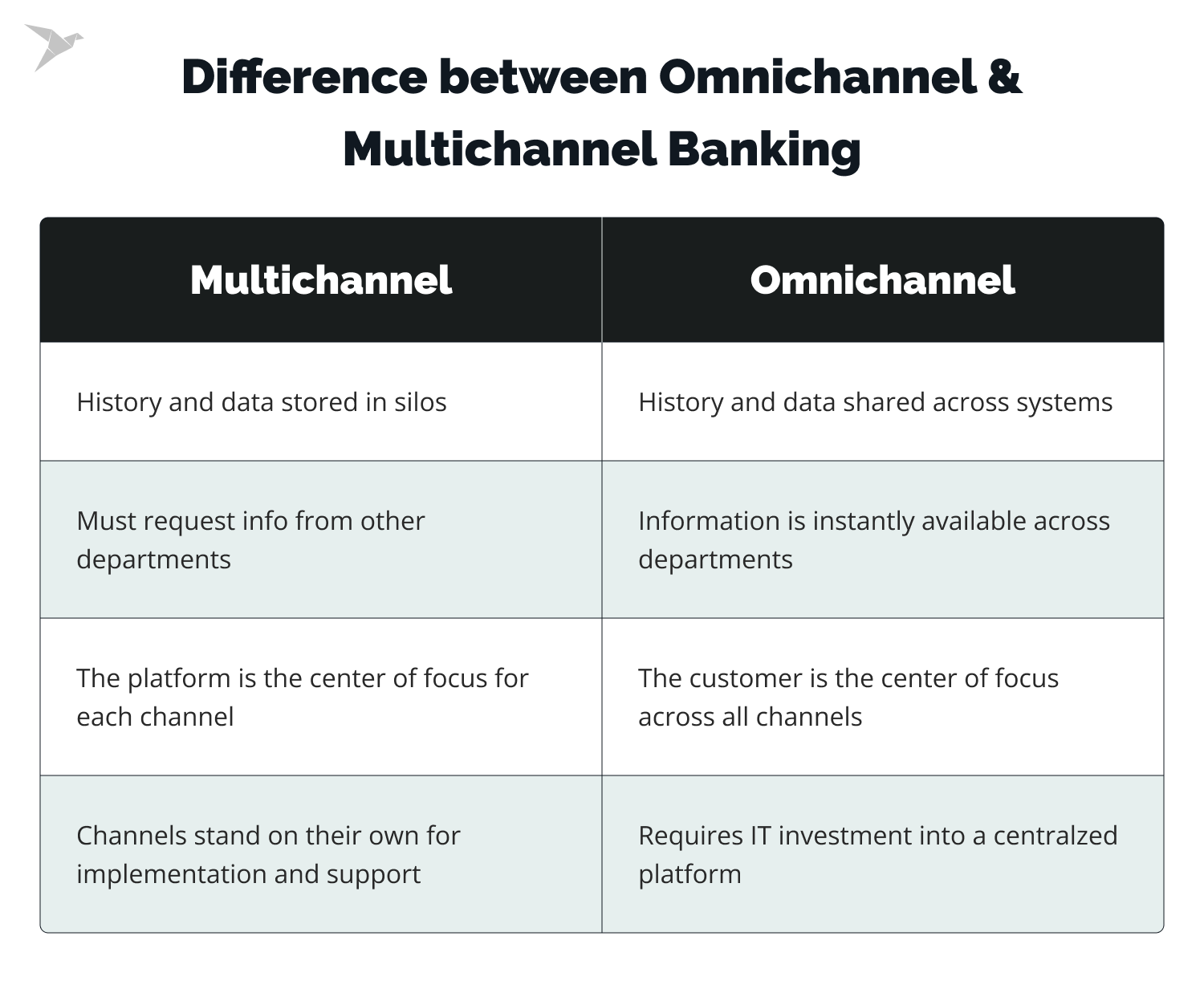

Difference between omnichannel and multichannel banking

In terms of customer experience, multichannel banking provides convenience through multiple channels, but consistency may be lacking. Customers may encounter difficulties transitioning between channels, resulting in a frustrating experience. In contrast, omnichannel banking enables seamless transitions in person interactions between channels, offering a unified view of customer interactions.

Multichannel banking, like omnichannel banking, involves offering various products and services across different channels such as in-branch appointments, ATMs, call centers, and mobile apps. However, the key difference lies in how these channels are integrated. In multichannel banking, these channels operate independently, focusing mainly on transactions rather than providing a seamless customer experience.

In omnichannel banking, customers can expect the same experience across all channels, whether using self-service options, speaking with a customer support agent, or engaging through text messages. Their preferences and information are seamlessly captured and displayed accurately in real-time across all channels.

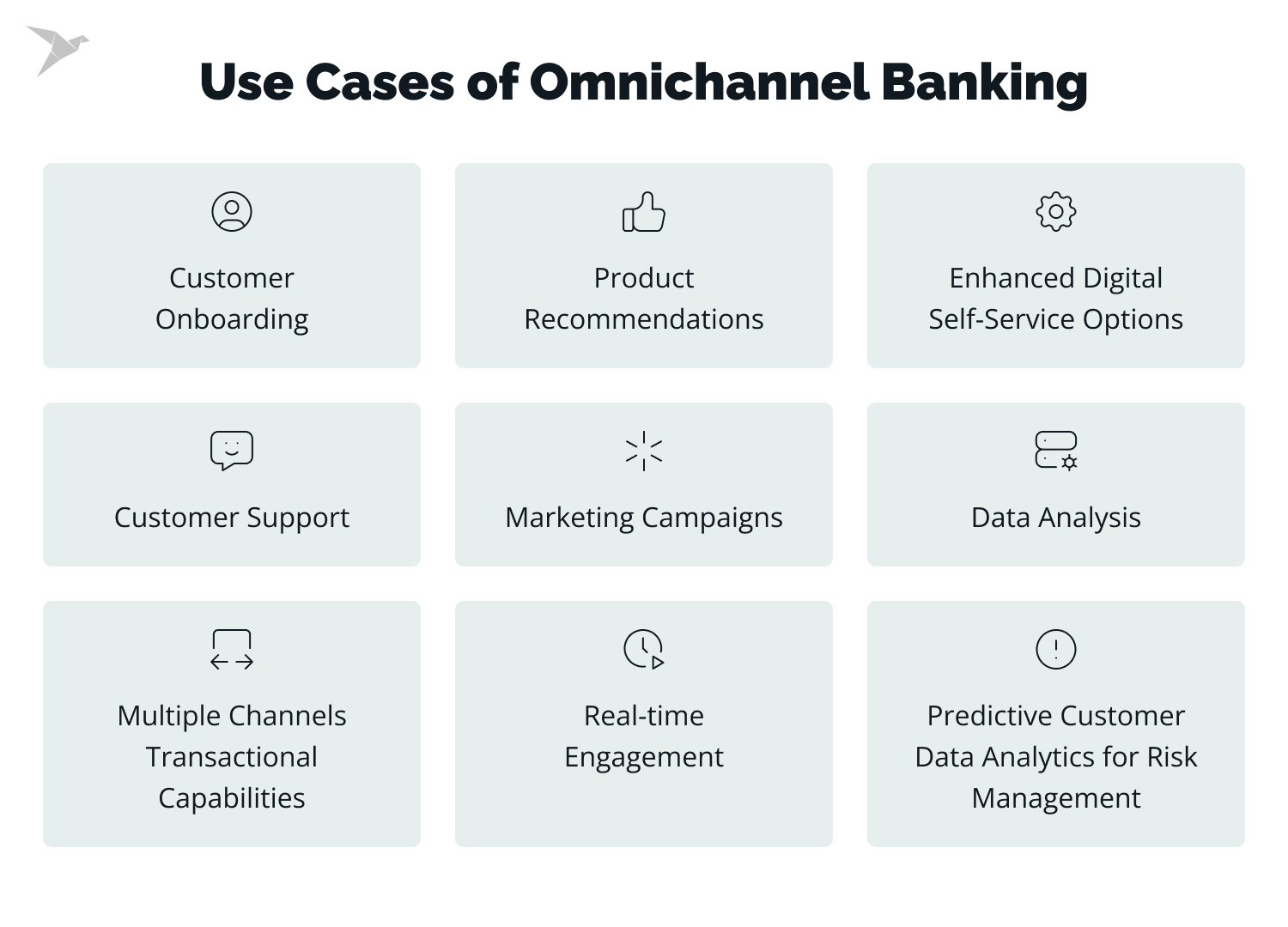

Use cases of omnichannel banking

Omnichannel banking presents many use cases that leverage its integrated approach to enhance customer experience, streamline operations, and drive business growth. Here are several key use cases of omnichannel banking:

Customer Onboarding

Omnichannel banking enables seamless customer onboarding processes by allowing customers to initiate account openings through various channels such as mobile apps, websites, or in-branch visits. Customer data is collected and synchronized across channels through a unified platform, eliminating the need for redundant data entry. This ensures a smooth and consistent onboarding experience regardless of the channel chosen by the customer.

Product Recommendations

By leveraging data analytics and machine learning algorithms, omnichannel banking platforms can analyze customer behavior and preferences across multiple digital touchpoints together. This enables banks to deliver personalized product recommendations tailored to each customer's unique financial needs and goals. For example, a customer browsing mortgage options on the bank's website may receive targeted offers for home loan refinancing through email or mobile notifications.

Customer Support

Omnichannel banking facilitates integrated customer support across various communication channels, including phone, email, live chat, and social media. A customer experiencing an issue with a transaction can seamlessly transition between channels while maintaining continuity in the conversation. Customer support agents have access to a unified view of the customer's interactions and history, allowing them to provide efficient and personalized assistance.

Marketing Campaigns

Omnichannel banking enables banks to launch contextual marketing campaigns that deliver relevant offers and promotions based on both traditional channels' static customer profiles, transaction history, preferences, and behavior. For example, customers who frequently use mobile banking to transfer funds may receive targeted promotions for a new mobile app or payment service. By delivering timely and personalized marketing messages across multiple channels, banks can increase engagement, drive conversions and commercial campaign conversion rates.

Multiple Channels Transactional Capabilities

With omnichannel banking, customers have the flexibility to initiate and complete transactions across multiple channels seamlessly. For instance, a customer can start a fund transfer on their mobile banking app, continue the transaction on the bank's website, and finalize it by visiting a branch office. This cross-channel transactional capability enhances convenience and flexibility for customers while ensuring consistency and accuracy in transaction processing.

Predictive Customer Data Analytics for Risk Management

Omnichannel banking platforms leverage advanced analytics and predictive modeling techniques to assess and from data effectively mitigate various risks, including fraud, credit defaults, and compliance violations. By analyzing customer data from multiple channels in real-time, banks can identify suspicious activities and anomalies, enabling proactive intervention to prevent fraudulent transactions and mitigate potential losses.

Enhanced Digital Self-Service Options

Omnichannel banking empowers customers with enhanced digital self-service options across various channels, including self-service kiosks, interactive voice response (IVR) systems, and chatbots. Customers can perform a wide range of banking transactions, such as account inquiries, bill payments, and fund transfers, without the need for human intervention. This reduces the workload on customer support staff and enhances operational efficiency.

Data Analysis

Omnichannel banking solutions offer robust data collection and analysis capabilities. With a unified architecture, banks can gather data from various sources, beyond direct channels, creating a comprehensive view of each customer. By applying analytics, including predictive analytics, banks can see customer journeys, gain insights into customer needs and anticipate their requirements, enabling proactive service delivery across channels.

Additionally, banks can utilize built-in analytics tools in omnichannel banking solutions to monitor customer behavior, identify upselling and cross-selling opportunities, develop new products, and respond promptly to market changes.

Real-time Engagement

Omnichannel banking provides real-time data to banks, allowing them to monitor customer interactions, preferences, and behaviors across channels. Through personalized notifications, instant messaging, and interactive chatbots, banks can engage with customers in real-time, addressing inquiries, resolving issues, and offering personalized recommendations promptly. This responsive approach ensures a seamless customer experience that meets the expectations of digitally connected customers.

Best Practices for Implementation

Implementing an omnichannel strategy isn't as simple as adopting a new tool—it requires a comprehensive transformation of the business approach, prioritizing the customer at the center. This presents challenges both technically and organizationally. So, where should implementation begin?

Firstly, ensuring seamless functionality across all channels requires centralized data access. Financial, personal, and marketing information must be consistent across web, mobile, telephone, and other platforms. This ensures that customers can seamlessly pick up where they left off regardless of the channel they use. Secondly, implementing such a strategy involves training employees to communicate across multiple channels effectively. It's not just about mastering new tools; it often entails overhauling customer service processes and potentially restructuring departments within the organization.

An important benefit of implementing an omnichannel strategy is the ability to analyze customer transaction data from various channels, systems, and social networks. Leveraging Big Data technology allows for collecting and analyzing information to create detailed customer profiles and understand their behavior. This granular customer data enables more accurate risk assessment, personalized advertising messages, and better matching of offers to specific customers, ultimately maximizing profitability in sales channels and generating greater profit.

Implement CRM systems to centralize customer data and track interactions across all channels. These systems enable banks to manage customer relationships effectively, track communication history, and tailor services based on individual preferences. By using data management capabilities integrating CRM with other banking systems, banks can ensure a seamless flow of information and provide consistent customer experiences.

Adopt an API-driven architecture to seamlessly integrate different banking channels, including mobile apps, websites, ATMs, and branches. APIs facilitate the exchange of data and functionality between disparate systems, allowing customers to access banking services across multiple channels without interruption. This approach enables banks to quickly adapt to changing customer needs and market trends.

Challenges and solutions in omnichannel banking implementation

Integration complexities

One of the primary challenges in implementing omnichannel banking is integrating disparate systems and technologies across various channels. Legacy systems, siloed data, and different technologies used in different channels can make integration complex and time-consuming.

Solution: To overcome integration complexities, banks can invest in modern technology platforms and middleware solutions that facilitate seamless integration across channels. Adopting APIs (Application Programming Interfaces) and microservices architecture can help decouple systems and enable faster and more flexible integration. Additionally, leveraging cloud-based solutions can provide scalability and agility in integrating new channels and functionalities.

Addressing cybersecurity concerns

With the expansion of digital channels and the increasing volume of customer data being transmitted across these channels, cybersecurity threats have become a significant concern for many banks and financial providers. Cyberattacks, data breaches, and fraud incidents can compromise customer trust and result in financial losses.

Solution: Banks need to prioritize cybersecurity measures to protect customer data and ensure the security of their omnichannel banking platforms. This includes implementing robust authentication and encryption mechanisms, regularly updating security protocols, and conducting thorough security audits and risk assessments. Investing in advanced cybersecurity solutions such as intrusion detection systems, behavioral analytics, and AI-powered threat detection can help banks detect and respond to security threats in real-time.

Staff training and change management

Implementing omnichannel banking requires not only technological changes but also cultural and organizational shifts. Staff members must adapt to new processes, technologies, and customer service approaches, which can be challenging and require comprehensive training and support.

Solution: Banks should invest in thorough staff training programs to ensure that employees understand the benefits of omnichannel banking and are proficient in using new technologies and systems. Providing ongoing support through digital training platforms and communication channels for employees to ask questions and provide feedback can help facilitate the transition. Additionally, fostering a culture of innovation and collaboration within the organization can encourage staff members to embrace change and actively participate in the omnichannel transformation journey.

Conclusion

Unlike previous generations, today's customers won't settle for one-size-fits-all treatment. They expect personalized service tailored to their preferences. With a robust multichannel infrastructure offering an omnichannel experience, banks can deliver seamless, personalized service across all touchpoints. It's time for banks to leverage the wealth of customer information available. In an increasingly digital world, seizing the omnichannel opportunity can be the difference between thriving banks and those left behind.

Omnichannel digital banking solutions is gaining traction across the industry. While banks and credit unions have been slower to adopt new technologies, more financial institutions are recognizing the benefits of omnichannel digital capabilities both in terms of cost savings and customer satisfaction

For further insights on transitioning to a fully omnichannel institution, don't hesitate to contact us. Let's work together to design a banking environment that embraces the future.

Interested to learn more about TechMagic?

Contact usFAQs

-

How does omnichannel banking enhance the customer experience?

Omnichannel banking improves the customer experience by providing seamless interactions across multiple channels. Customers can start a transaction on one channel and continue it on another without interruption.

-

What are the key benefits of implementing omnichannel banking?

The key benefits of implementing omnichannel banking include enhanced customer satisfaction, improved retention rates, increased operational efficiency, sales productivity, and higher revenue generation. By offering a consistent and personalized experience across channels, banks can strengthen customer relationships, attract new customers, and drive growth.

-

What challenges may arise during omnichannel implementation, and how can they be addressed?

Challenges during omnichannel implementation may include legacy system integration, data management issues, cybersecurity threats, performance management and staff training needs. These challenges can be addressed through careful planning, investment in robust technology infrastructure, prioritizing data integration and security measures, and providing comprehensive training and support for sales teams and staff.

-

Can small banks implement omnichannel strategies effectively?

Yes, small banks can implement omnichannel strategies effectively by leveraging technology solutions that are scalable and adaptable to their needs. While small banks may have limited resources compared to larger institutions, they can still prioritize customer-centric approaches, invest in user-friendly digital channels, and partner with experienced vendors to implement omnichannel solutions tailored to their specific requirements.

linkedin

linkedin

facebook

facebook

twitter

twitter