TechMagic Academy

TechMagic AcademyDigital Banking Transformation: An Overview

Last updated:27 December 2023

From the days of paper-based transactions to the current era of AI-driven personalization, the transformation in banking is palpable. We'll dive into the drivers behind this shift, the challenges faced by the industry, and the extraordinary opportunities that digitalization presents.

A 30 percent of banks that embark on a digital transformation journey successfully realize their digital strategy, leaving the majority falling short of their intended objectives.

According to a report by MarketsandMarkets, the global digital banking platform market is poised for remarkable growth, projected to surge from USD 8.2 billion in 2021 to USD 13.9 billion by 2026, with a Compound Annual Growth Rate (CAGR) of 11.3%. This expansion is primarily attributed to the demand among banks to provide an exceptional customer experience and the increasing integration of cloud technologies in banking institutions.

Approximately 2.5 billion individuals will benefit from online banking services by 2024, in contrast to 1.9 million in 2020. Noteworthy examples of digital banking transformation include online banking applications, robust data encryption software, virtual assistants, KYC system software, and more. These innovations collectively contribute to an enhanced and customer-centric digital banking experience.

Why would a well-established financial institution invest billions in technology? The answer lies in:

- Meeting the ever-increasing demand for seamless, personalized, and digital banking experiences challenges traditional banks to adapt to changing customer preferences.

- Navigating a complex web of regional and evolving financial regulations.

- Safeguarding customer data and financial transactions in an era of heightened cyber threats and data breaches requires substantial investments in cybersecurity.

- Outdated and inflexible legacy systems can hinder the ability to adapt to modern technology and may prove costly to maintain, posing challenges to innovation and efficiency.

For consumers, the appeal of fintech is straightforward – convenience. Fintech products simplify their lives by boasting AI-driven personalization and seamless digital account openings. Failure to align with these technology-driven services places traditional banks at risk of losing their competitive edge and market share.

The foundational approach to digitalization within the banking and fintech sectors revolves around comprehending customer behavior, preferences, and demands. Consequently, the banking industry has shifted from being product-centric to adopting a customer-centric approach.

As the public increasingly gravitates towards online shopping and mobile applications, banks have had to reconfigure their operational paradigms to gain a competitive edge. Achieving digital transformation in the banking sector necessitates a comprehensive digitization strategy encompassing everything from customer engagement to revamping backend operations.

The shift from traditional to online banks

Today, banks rely on omni-channel strategies to revolutionize the customer journey. The transition to digital services has not only improved operational efficiency but also facilitated growth by reaching a broader pool of potential customers.

Banks have come to realize that direct competition with fintech companies may not be the most effective strategy. Instead, a more promising approach lies in exploring innovative forms of collaboration that deliver enhanced value to customers. One example is the adoption of cloud-based alternatives, which involve replacing traditional IT systems with more agile and adaptable solutions.

What is digital transformation in banking?

Digital transformation is the compass guiding the operational and cultural shift toward the comprehensive integration of digital technology across all facets of the banking landscape. This profound transformation is geared towards optimizing internal operations and, most crucially, enhancing customer value delivery. When executed with precision, digital transformation becomes the catalyst that empowers banks to not only survive but thrive in an increasingly competitive market.

Undoubtedly, technology serves as the backbone of this transformation. However, it's important to understand that technology alone is not a magical panacea. Success in digital transformation hinges on an approach that transcends technology deployment. Banks must be astute in selecting the right technologies and orchestrating their strategic implementation to reap the tremendous benefits. Moreover, they must confront the cultural challenges and ingrained mindsets that often impede an organization's ability to embrace and adapt to new technologies.

Although the core principles of banking remain consistent, how the industry engages with customers has evolved. New entrants in the financial sector, such as fintech companies and neobanks, are offering highly personalized experiences that empower customers to take greater control of their finances.

Examples of digital transformation in banking include the introduction of digital account opening for both consumers and businesses, digital loan origination systems, person-to-person (P2P) and real-time payment solutions, and the automation of marketing and customer relationship management (CRM).

Digital transformation in the banking sector comes with challenges, including regulatory compliance and cybersecurity concerns. Banks must remain vigilant in adhering to know-your-customer (KYC) and anti-money laundering (AML) best practices and privacy regulations such as GDPR.

Importance of digital transformation in banking and financial services

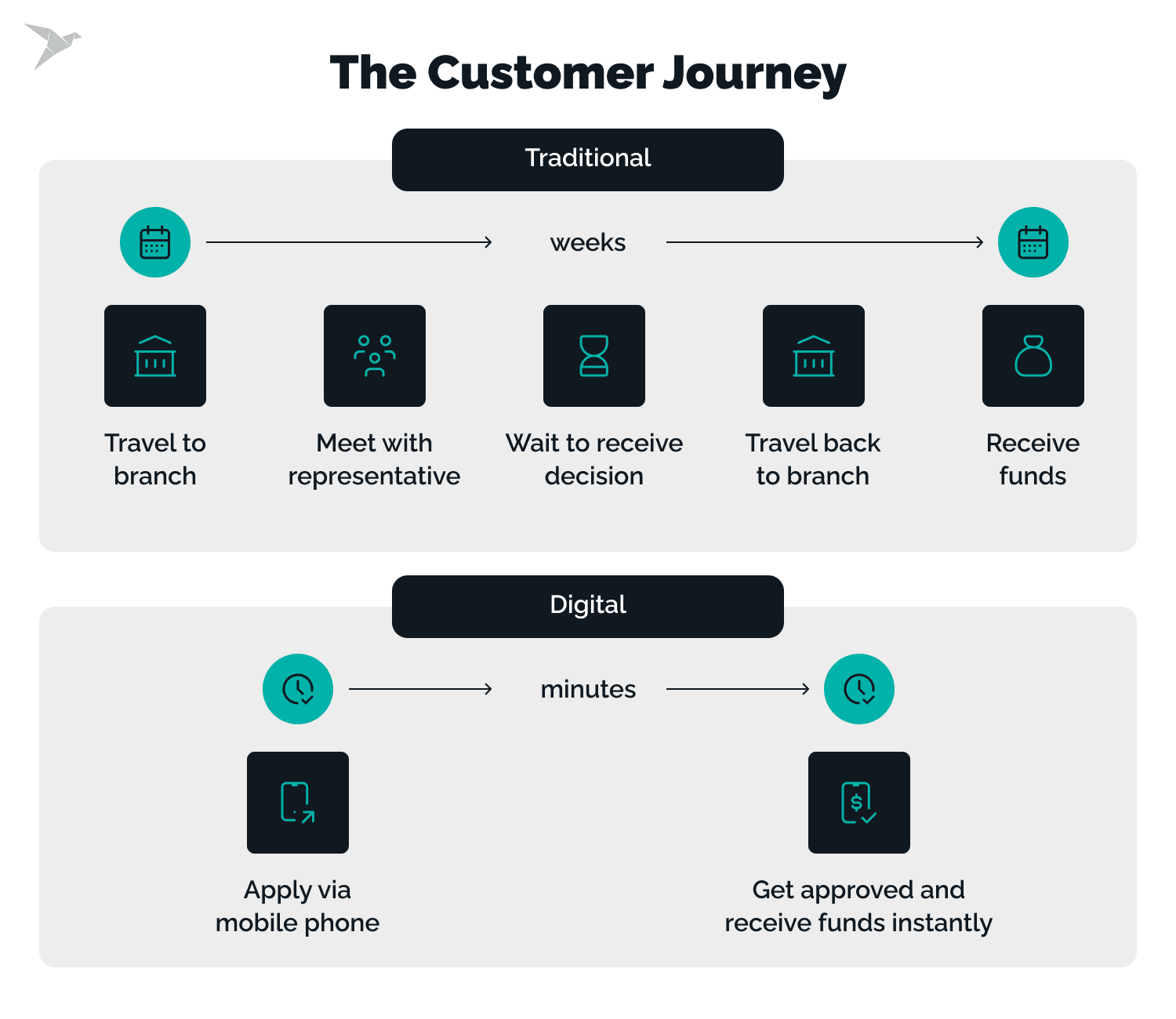

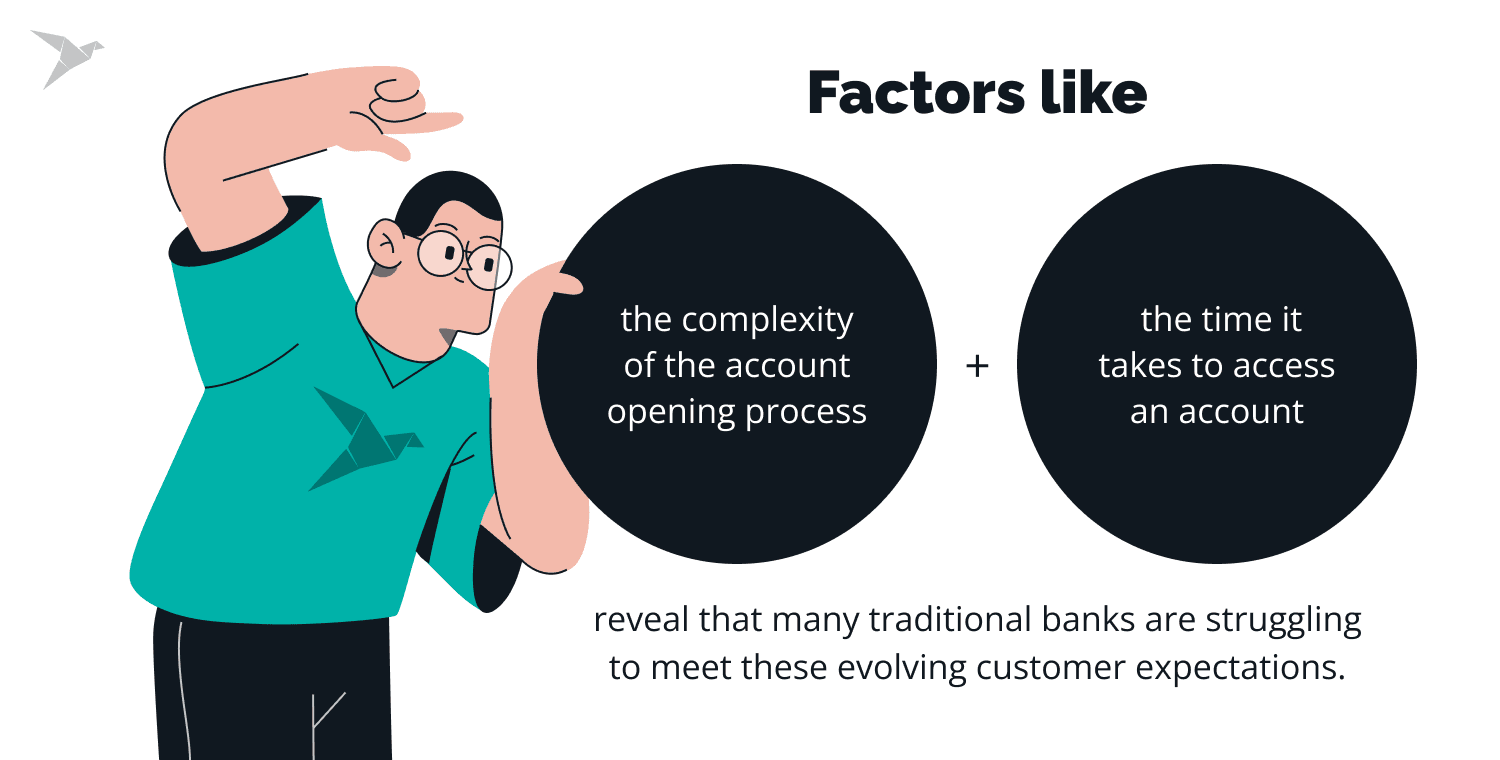

In today's rapidly changing digital landscape, customers' expectations have shifted significantly due to the seamless, on-demand experiences offered by industry giants such as Amazon, Uber, and Netflix. As a result, banking customers now anticipate similarly efficient and user-friendly services from their financial institutions. An illustrative case study underscores the gap between challenger banks and traditional ones regarding the customer experience when opening a bank account.

When opening an account or making a payment becomes overly cumbersome, customers are likelier to abandon their efforts. In fact, as much as 43% of potential customers may give up on the sign-up process due to excessive duration, convoluted steps, or an excessive request for personal information, according to PwC research.

Digital disruption stands out as the foremost catalyst for the pressures weighing on traditional banks and financial institutions. Goldman Sachs estimates that these disruptions could result in an annual revenue loss of $4.7 trillion for traditional financial institutions. These disruptions manifest in various forms, stemming from innovative startups, advancing technology, market dynamics, and government regulations.

Complex Regulatory Compliance

Compliance with Know Your Customer (KYC) regulations is essential for any bank. However, staying compliant with regulatory requirements often demands a significant allocation of resources, frequently necessitating dedicated teams to oversee these efforts. While this situation is unlikely to change in the foreseeable future, there is room for improvement. The lack of automation and digitization in this realm continues to strain business resources, with many organizations viewing compliance as a mere checkbox exercise rather than an opportunity for innovative approaches.

Digital Threats and Fraud

Opportunities for businesses and customers have expanded, as have the avenues for exploitation. The shift to digital processes exposes businesses and customers to new threats, including online identity fraud and security vulnerabilities like data breaches. Historically, the banking sector is a prime target for fraud and financial crime and is prepared to contend with these attacks. However, it must also anticipate a fresh wave of fraudsters that inevitably accompany digitization initiatives.

Legacy Systems and Mindsets

Digital-first banking applications have been pivotal in propelling digital transformation within the banking industry. New market entrants, capable of swift innovation, have encroached upon market share, prompting many banks to recognize the necessity of embracing innovation and new technologies for competitiveness. Despite possessing the necessary resources, these banks grapple with the inertia of legacy systems and mindsets, which can impede the pace of digital adoption.

Customer experience

Customers have raised the bar for what they expect. They increasingly seek a top-tier cross-channel experience with personalization, data-driven insights, and seamless end-to-end customer journeys. Banking clients now anticipate the flexibility to access services online and through their preferred devices.

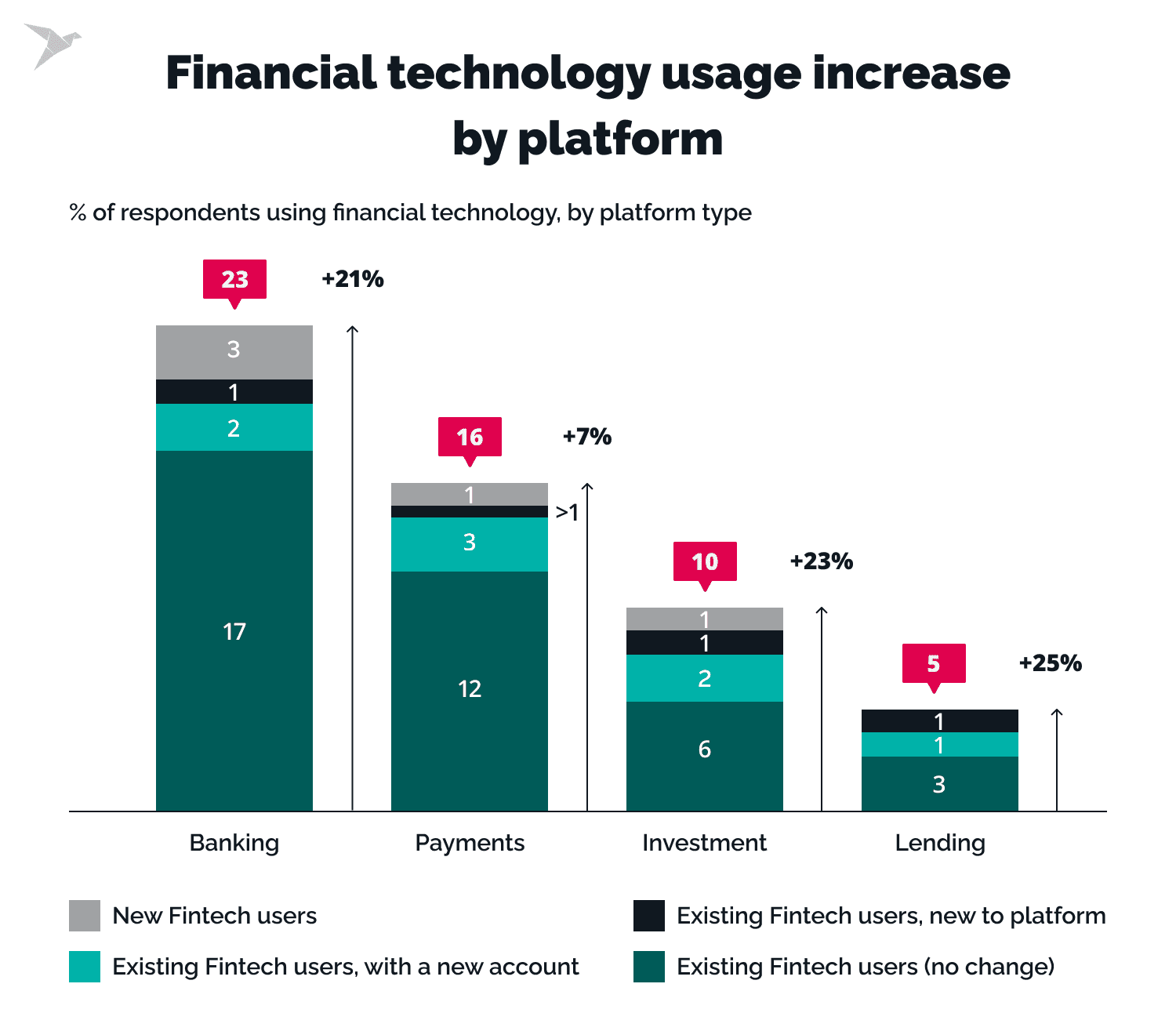

For instance, only 17% of U.S. bank customers opt for in-branch transactions, with 46% preferring the convenience of online banking and 30% favoring mobile options.

PwC's findings from 2021 reveal that a significant 61% of U.S. consumers utilize digital banking channels every week.

Competition for Market Share

While 47% of bank and credit union executives consider fintech companies to be formidable contenders, the perceived threat posed by neobanks has somewhat diminished, with just 21% of executives seeing them as a concern in 2023, down from 33% in 2022.

However, banks are not merely competing with fintech companies and neobanks; they are also in a race with their peers within the industry. Over three-quarters of banks have already crafted digital transformation strategies, and over 18% plan to roll out their strategies in 2023.

Influence of Data on the Customer Journey

At each stage of a customer journey, data plays a pivotal role, either enhancing or detracting from the overall experience. Data analytics, for instance, facilitates precise microsegmentation and omnichannel personalization, enabling banks to offer timely and highly targeted customer offers. Meanwhile, data-driven automation expedites numerous front-office processes, heightening customer satisfaction.

Operational Efficiency

The digital transformation of banks extends to data standardization and streamlining straight-through processing, effectively reducing the risk of human error and automating repetitive tasks. The transition from legacy systems to flexible, composable architecture solutions can substantially reduce IT operational costs, potentially reaching a 50% decrease.

Learn how we built macro-investing app with its own token and reward system

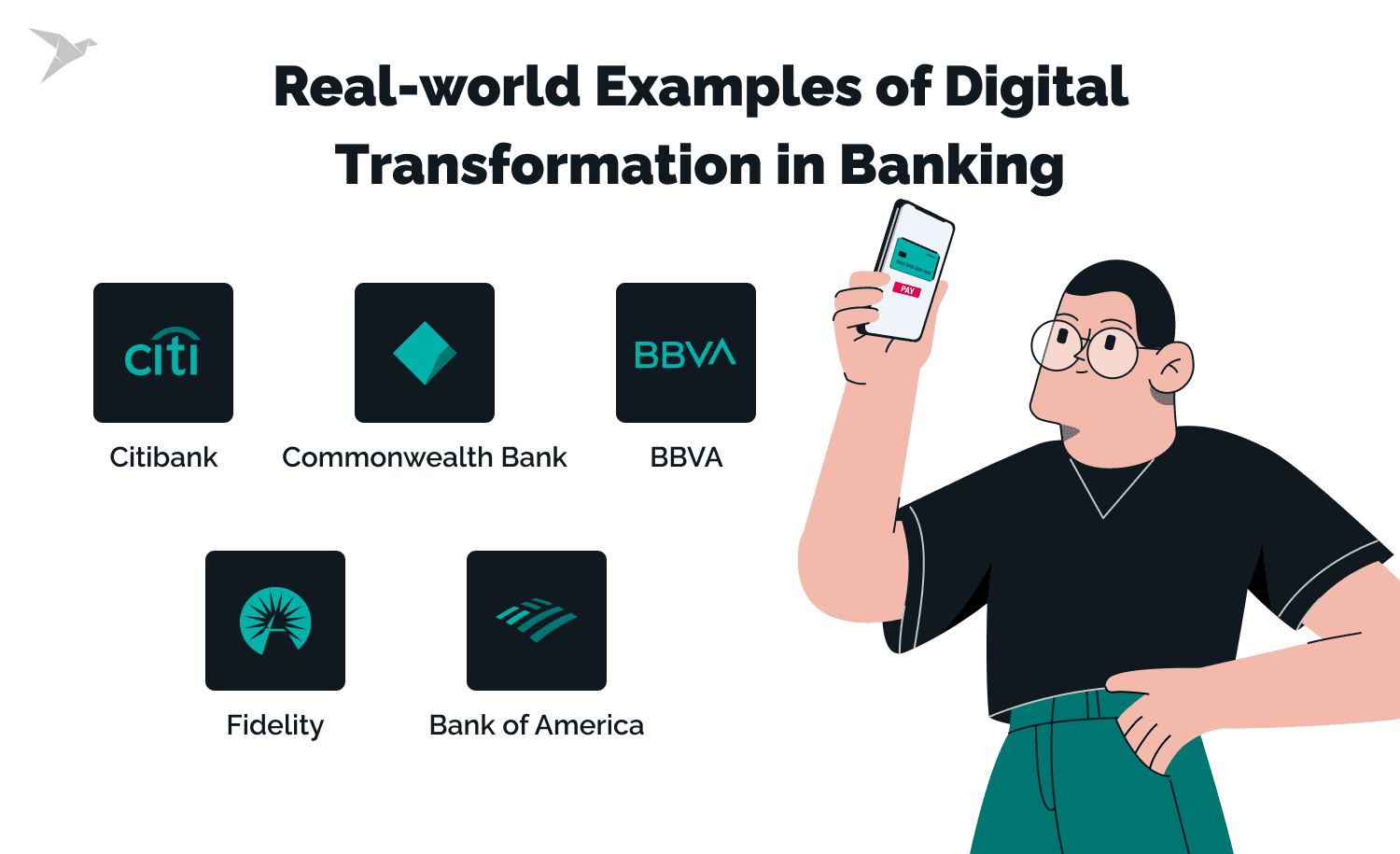

Real-world Examples of Digital Transformation in Banking

Citibank

Citibank is one of the first banks in the USA that identified the surging popularity of mobile banking apps. In response, the institution implemented a mobile-first approach, prioritizing mobile banking as a core solution rather than a supplementary offering to physical branches or web-based services.

BBVA

BBVA, a prominent banking institution, strategically empowered customers to independently address their banking needs, reducing reliance on staff intervention. Impressively, nearly 94% of BBVA's product and service portfolio operates on the Do-It-Yourself (DIY) model. This strategic shift not only reduced costs but also streamlined customer interactions, enabling employees to concentrate on offering consultation and guidance for more complex transactions.

Fidelity

Fidelity has introduced robust digital investment platforms that empower users to manage their portfolios efficiently. Through intuitive interfaces and advanced analytics, customers can access real-time market data, make informed investment decisions, and execute trades seamlessly.

Leveraging AI and machine learning algorithms, Fidelity delivers personalized financial guidance to its clients. Advanced encryption, multi-factor authentication, and continuous monitoring protect customer data and transactions, fostering trust and confidence among users.

Bank of America

Bank of America introduced a suite of customer-centric products that resonated profoundly with consumers:

- Zelle, a real-time payment app with 16 million active accounts as of January 2022 and a record-breaking 514 million transactions in 2021.

- Erica, a virtual financial assistant fueled by AI, sought out a staggering 659 million times in 2021.

- Life Plan, a personal finance app that has garnered over 10 million clients since its inception in 2020.

- CashPro Forecasting, a tool designed for predicting future cash positions, aimed at Bank of America's commercial clients, and will introduced in 2022.

Commonwealth Bank

The Commonwealth Bank, a prominent Australian multinational banking institution known as CommBank, has earned accolades for its mobile banking app, widely acknowledged as the finest banking app not only in the country but across the globe. Its distinctiveness lies in its extensive customization features, high personalization, and robust security with location-based functionalities. The app is further fortified by machine learning capabilities, facilitating the delivery of three billion personalized messages annually.

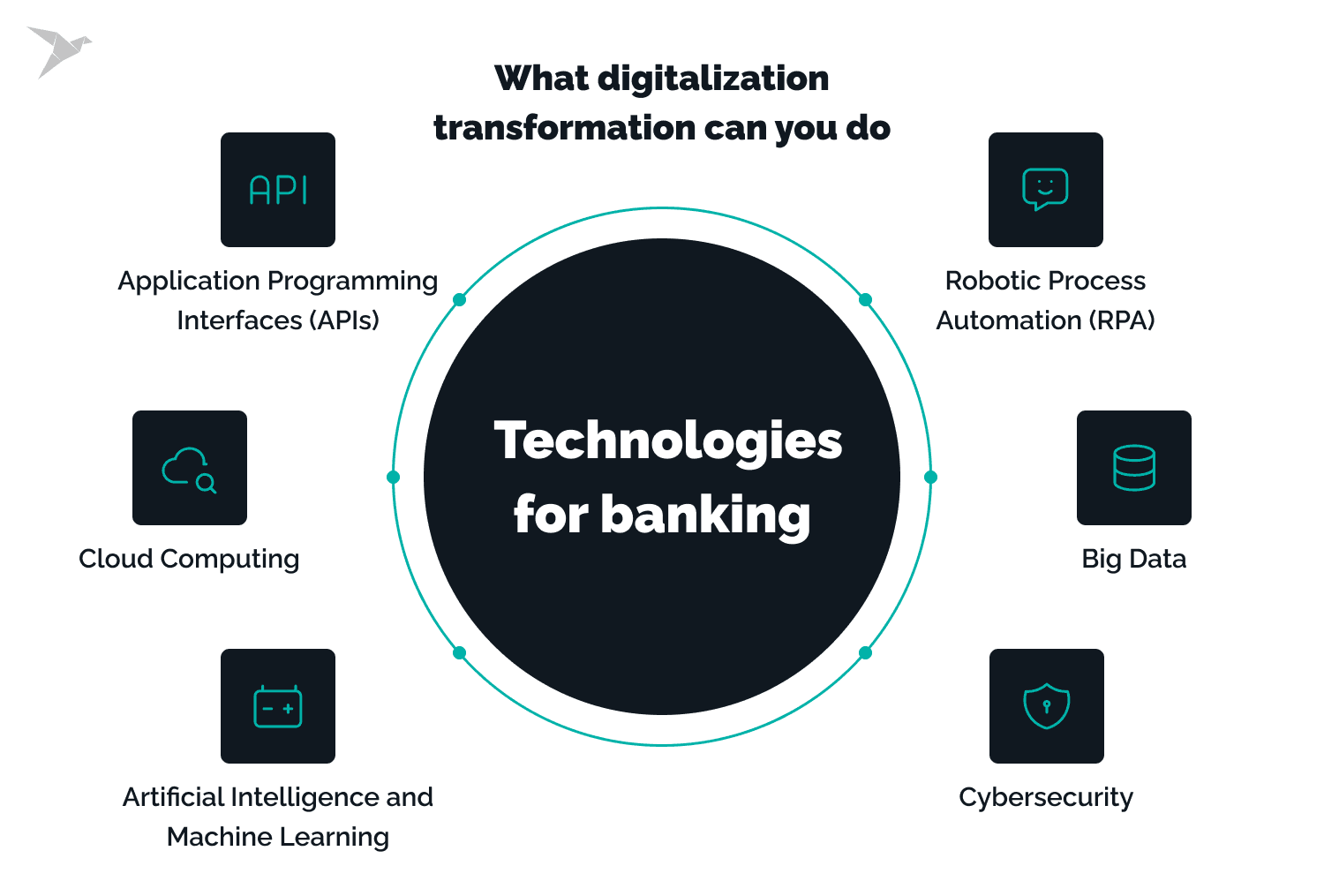

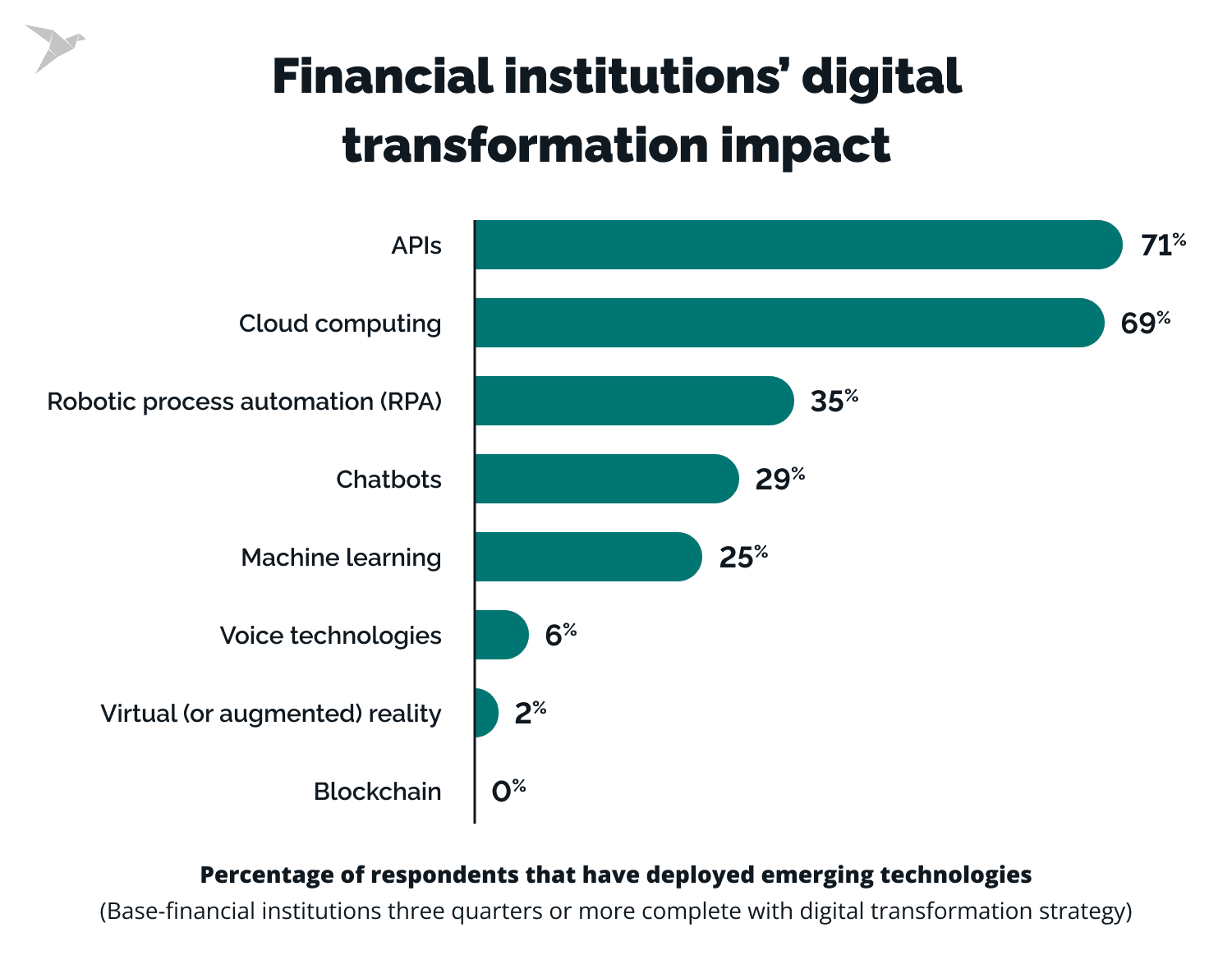

What Digitalization Transformation Сan You Do: Technologies for Banking

Application Programming Interfaces (APIs)

71% of financial institutions embarking on or having already completed their digital transformation journey have strategically deployed APIs.

APIs have surged in popularity, largely due to the concept of open banking, which has gained solid ground in the European Union and Asia-Pacific regions. Facilitated by APIs, open banking entails the seamless sharing of financial data between fintech companies, banks, and other institutions.

Open banking powers a host of innovative features, such as bank account synchronization in budgeting apps (e.g., Mint), streamlining lending and digital account opening processes, and enhancing personalization.

Cloud Computing

Among financial institutions near the increase of their digital transformation (DT) strategies for boosting operational efficiency, facilitating resource accessibility, and seamlessly supporting a distributed workforce, 69% have already transitioned to cloud computing.

The pervasive adoption of cloud computing is attributable to several compelling advantages:

- Scalable Infrastructure: The flexibility to scale resources seamlessly eliminates the hassles of unexpected downtime and subpar performance that can vex customers.

- Continuous Delivery (CD): Updates to the bank's systems can be executed without any downtime, ensuring uninterrupted service.

- Cost efficiency: Financial institutions can pay for the resources they use without the burden of maintaining infrastructure components like servers and data centers.

Robotic Process Automation (RPA)

RPA leverages rule-based software to automate specific business processes. RPA tools simplify the automation of repetitive and labor-intensive manual tasks, thanks to their low-code scripting capabilities. Incorporating RPA can pare down processing costs by up to 70%. For instance, RPA can play a pivotal role in customer service by swiftly addressing customer concerns.

RPA brings forth many benefits, including productivity, reduced labor costs, improved employee job satisfaction, and the mitigation of human errors. Notably, RPA can be integrated with an add-on that seamlessly integrates with existing systems.

RPA can be effectively applied to tasks such as:

- Data entry and extraction

- Basic customer service communications

- Trade booking and processing

Artificial Intelligence and Machine Learning

AI plays an increasingly vital role in the digital transformation of banking institutions. It can be an online assistant and chatbot, offering customers real-time communication options to address common inquiries and provide essential information without needing customer service representatives.

In addition to customer-facing applications, AI in banking supports data analytics and automation, enabling financial institutions to identify patterns in customer behavior, pinpoint opportunities, and streamline their operations. Machine learning is also gaining prominence in fraud protection, effectively detecting anomalous activities and implementing automated preventive measures to safeguard customer accounts.

AI solutions are further advancing digital transformation in investment banking, with AI technologies offering investment recommendations based on customer profiles, factoring in variables such as risk tolerance, investment horizons, historical performance, and more to present potential options.

Check out what TechMagic did for cryptocurrency live data aggregator with real-time visualization of the crypto market.

Big Data

Big data analytics empowers financial institutions to gain deeper insights into their operations and customer base, thereby creating opportunities for optimization. Big data in banking leverages customer data to enhance sales efforts by identifying products or services that address specific customer pain points and ensuring tailored recommendations.

Risk management is another area where big data shines, simplifying identifying problematic patterns, monitoring feedback, and assessing customer sentiment. This capability allows financial institutions to take appropriate actions to reduce fraud and maintain their reputations.

Cybersecurity

Cybersecurity remains a central concern in banking, encompassing regulatory compliance and general data and account security. Data breaches or financial theft not only harm an institution's reputation but can also lead to legal consequences related to regulatory compliance failures.

Furthermore, banks typically store highly sensitive data, including personally identifiable information (PII) of their customers. Even if a breach does not involve the theft of funds, it can provide malicious actors with the means to exploit PII for identity theft, which can be equally or even more detrimental than financial losses.

Effective cybersecurity practices enable financial institutions to proactively address and mitigate security risks, ensuring the proper protection of customer and company data and assets against theft, tampering, and other malicious manipulation.

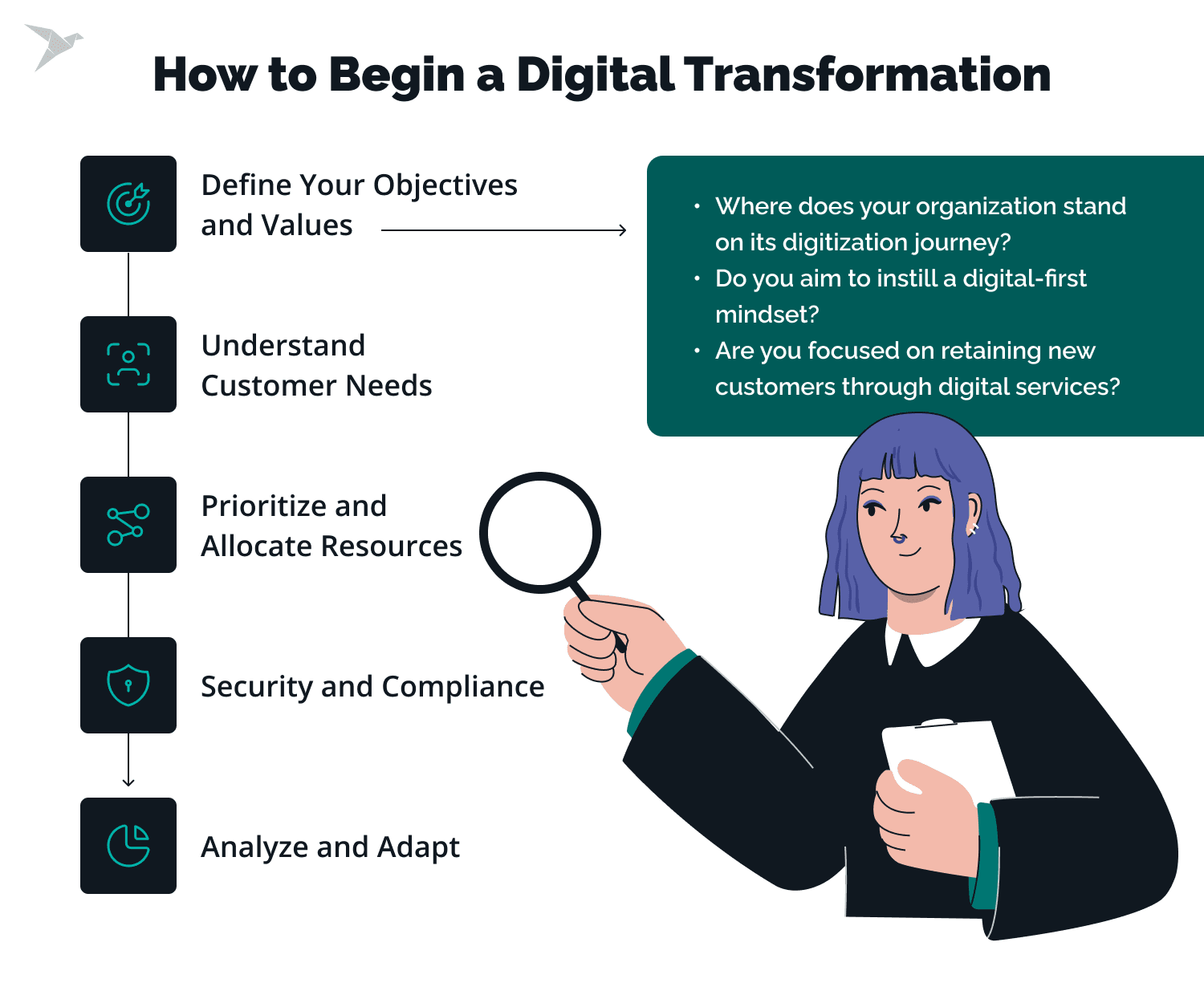

How to Begin a Digital Transformation

Digital transformation within the banking sector is a multifaceted journey that demands meticulous planning and execution. To guide you on this path, here are key steps that banks can adopt to ensure a successful digital transformation:

Define Your Objectives and Values

Start by mapping out your goals and create a comprehensive plan to achieve them. Begin by analyzing your organization's current state, processes, and technologies already in place.

At this crucial stage, it's essential to ask the right questions.

- Where does your organization stand on its digitization journey?

- Do you aim to instill a digital-first mindset?

- Are you focused on retaining new customers through digital services?

Be specific. In banking, digital transformation encompasses three core pillars: customer-centricity, integration, and inclusivity. Through technology, the customer journey is personalized, automated, and seamlessly woven into a unified ecosystem.

The ultimate aim of digital transformation is a deep understanding of and responsiveness to customers' needs. For example, a mobile application becomes a versatile tool, serving customers in bill payments, online money transfers, loan applications, and instant information access at their fingertips.

This level of convenience not only fosters robust customer retention but also trims the costs associated with customer acquisition, streamlines onboarding processes, and bolsters revenue.

Digital transformation can take various forms, from technological upgrades to procedure changes. Focusing on specific objectives ensures resource management is optimized and provides a clear organizational priority.

Understand Customer Needs

Prior to implementing changes, it's essential to comprehend the current customer journey thoroughly. Mapping out the steps customers must take for various actions allows banks to identify pain points and set clear goals for digital transformation.

Beyond mapping customer journeys, data analytics can provide insights into transaction timelines, highlighting improvement areas. Direct customer feedback is equally invaluable, as it helps pinpoint the changes that offer the most perceived value.

Prioritize and Allocate Resources

Remember that digital transformation is a long journey, best tackled in incremental steps. Once you have a refined list of objectives and goals, assess your resources and prioritize them based on specific tasks. This allows you to make the most efficient use of your time, budget, and human resources. Identify quick wins and avoid overwhelming your team with numerous simultaneous changes. Implement these changes incrementally, starting with small successes.

Conduct a thorough inventory of your entire technology stack, including currently underutilized features. This evaluation enables you to determine how to maximize your existing resources and pinpoint the genuine gaps. Consequently, you can pinpoint areas for improvement that promise the most substantial results with prudent investments, ensuring a strategic and cost-effective digital transformation.

Security and Compliance

Recognize that the banking industry often exhibits resistance to sweeping changes. Therefore, dedicating time to securing buy-in across all organizational levels is essential. Leaders, managers, and technology professionals who will play pivotal roles in the transformation must fully align with the endeavor.

Banks navigate a complex regulatory landscape, adhering to stringent standards such as Know Your Customer (KYC), Anti-Money Laundering (AML), and General Data Protection Regulation (GDPR). Compliance with these regulations is non-negotiable and forms the cornerstone of operational integrity and customer trust. Implementing robust measures to ensure compliance is integral to successful digital transformation.

Banking institutions must unify efforts to fortify their infrastructure, processes, and technologies. A collective commitment to security and compliance not only mitigates risks but also fosters a foundation of trust among stakeholders in an ever-evolving financial landscape.

Analyze and Adapt

Once your transformation plan is in motion, taking a step back to analyze your efforts and evaluate their impact is essential. Success should be defined by how much you've achieved your initial goals. If you've succeeded, congratulations are in order!

However, if your efforts haven't yielded the desired results, it's not a setback, but an opportunity to make necessary adjustments. Gather feedback from your team, refine your processes, and continue working to ensure your digital transformation is a resounding success.

As implementation draws near, introduce the transformation concepts to your customers through a gradual, bite-sized approach. Customers can acclimate themselves to the impending changes by employing a drip campaign-style strategy. This not only aids in customer readiness but also elevates the overall customer experience, expediting the adoption process.

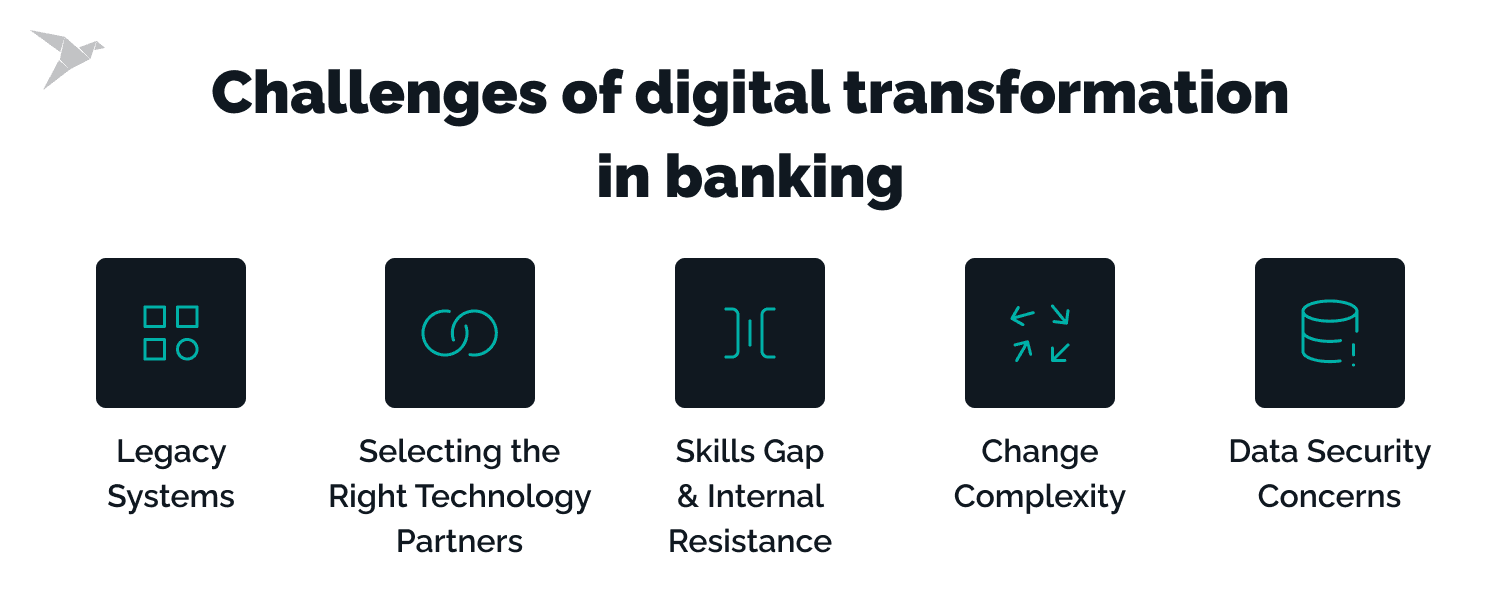

Challenges of digital transformation in banking

The banking industry is experiencing a slower pace of change than its innovative counterparts, with large banks often trailing behind in innovation and productivity. Their reliance on traditional operating models and limited adoption of agile work methods can impede the success of their digital transformation efforts. A McKinsey survey conducted in 2021 revealed a significant discrepancy: while fintechs and neobanks introduce new product features every two to four weeks on average, traditional banks tend to have longer product rollout cycles, typically spanning four to six months.

Despite the many advantages associated with digital transformation in banking, the path is not devoid of challenges:

Legacy Systems

Another area of concern is the legacy systems still prevalent in many banks. Outdated software and technology, such as the enduring COBOL programming language, persist in major banking systems. A Forbes survey underscores the reality, with nearly 60% of banks relying on legacy mainframes aged 5 to 10 years. An additional 27% cope with equipment that's 11 to 20 years old, while 9% manage equipment dating back 21 to 30 years.

The outdated systems are ill-equipped to handle the current digital age's traffic volume and diversity, necessitating a much-needed upgrade. Transitioning from these legacy systems to modern, integrated solutions is a challenging and time-consuming. Legacy applications in universal banks often average around 14 years old, while digital banks operate with much newer systems, averaging only three years old.

Integrating contemporary digital technologies with legacy systems can be intricate, time-intensive, and capital-intensive. Banks must possess the right technology and infrastructure to efficiently gather and analyze data. Legacy systems often contribute to data silos, where outdated computer systems and software create a challenge when integrating data from various sources. This results in data being fragmented in separate databases or unconnected systems.

Selecting the Right Technology Partners

Digital transformation in banking necessitates a blend of in-house and external talent, financial resources, and time. Underestimating the extent of these resources often leads to project delays, budget overruns, or, in some cases, project failures.

Banks must exercise prudence in their choice of technology partners. These partners must offer technology solutions conducive to delivering a seamless, cross-channel customer experience and are capable of helping banks meet regulatory requisites. Alignment with strategic goals is paramount, as are commitments to collaborative partnership and shared objectives.

Skills Gap and Internal Resistance

A prevalent challenge is the glaring gap in digital skills. Many organizations acknowledge this as a significant barrier impeding their digital transformation aspirations. Urgent actions are required from educational institutions, capacity-building organizations, and all stakeholders to revamp their training programs and address this shortage.

The success of digital transformations hinges on profound cultural and behavioral changes within organizations. This encompasses fostering calculated risk-taking, enhancing collaboration, and embracing a customer-centric ethos. Resistance to these shifts can undermine the success of digital transformation initiatives.

Change Complexity

Executives sometimes underestimate the complexity of change required for a meaningful digital transformation in banking. This oversight can lead to a misjudgment of resource needs and an inefficient transformation process.

- A digital strategy typically commences with a business case, calculated with a specific timeline for impact. When transformation initiatives exceed the initially projected timeline, the increase in cost often surpasses the expected value. It's a common occurrence, with over half of digital banking transformations exceeding their original timeline and budget, or in some cases, failing.

- Addressing technical debt, encompassing legacy technology stacks, unused applications, and redundant infrastructure, is often overlooked in initial transformation budgets.

Data Security Concerns

Data security is a linchpin for two pivotal reasons: Customers and Compliance. Studies indicate that data protection ranks as the primary driver for customers switching banks or credit unions. Furthermore, non-compliance with privacy and data security regulations can place banks in precarious situations with regulatory authorities. Unfortunately, traditional banking systems can be vulnerable to cyberattacks and data breaches, which can jeopardize by shield customer data and prevent unauthorized access to the security of sensitive data.

A comprehensive strategy involves a layered approach to data security, including encryption to protect data regardless of its location, the implementation of multi-factor authentication, and the establishment of secure processes for continuous testing and security enforcement.

Embrace Digital Transformation of Your Banking With TechMagic

The pressure on the financial services industry to deliver a digital-first customer experience is greater than ever.

Digital transformation in banking is not a mere integration of digital channels; it entails the creation of an entire digital ecosystem designed to cater to the evolving needs of customers. Embracing a digital mindset empowers organizations to pivot towards customer-centricity, understanding and meeting customers' ever-changing requirements. The report indicates that 70.5% of executives identify enhancing customer experience as the driving force behind their digital transformation, in contrast to 28% who view it as a means to access new technologies. Failing to adapt to this technological shift can result in inefficiencies, loss of market share, and a lag behind industry peers.

It's with its challenges, especially for the global banks with their intricate legacy systems. The adoption of new, digitized customer journeys presents a myriad of complexities that demand expert navigation.

With over 9 years of experience, we have consistently supported financial institutions in modernizing their digital ecosystems. To illustrate how we facilitate banks in upgrading legacy systems and unlocking the potential of cutting-edge technology, contact us to discuss the custom digital transformation solution for your banking.

The time for hesitation is over – the time to initiate your banking digital transformation journey is now.

FAQ

Digital transformation is paramount for the banking industry to stay competitive and meet the evolving needs of customers. Its primary goals are to enhance customer experience, streamline operations, reduce costs, and remain agile in a rapidly changing financial landscape.

The initial steps in a bank's digital transformation journey involve clearly defining objectives, aligning them with the organization's strategy, and securing leadership buy-in. These steps are essential to set a clear direction, secure resources, and ensure the transformation is purpose-driven.

Banks can maintain data security and compliance by implementing robust cybersecurity measures, adopting encryption, and regularly auditing their systems. Compliance with industry regulations and data protection laws is also crucial, necessitating the integration of compliance considerations into the transformation process.