Revolutionising Banking: The Best Open Banking Apps

Years passed when traditional banking was the only option for managing your finances. With the rise of open banking, consumers can now access various innovative apps and services that offer a more personalised and streamlined banking experience.

Open banking banks revolutionize with a wide range of services, including rapid payments, budgeting, investments, and the verification of credit status and income.

Whether you're looking to simplify your budget, track your spending, or invest your savings, these open banking apps are created to help you make smarter financial decisions. With the added convenience of mobile banking and digital transactions, you can manage your money from anywhere, anytime.

In this post, we'll explore the top open banking market, advantages, solutions, best apps, and how open banking APIs work.

Understanding Open Banking: Benefits and Existing Solutions

Open banking refers to a financial practice that allows different financial institutions to share customer data and collaborate on services through application programming interfaces (APIs).

With a customer's permission, their financial data can be shared securely and seamlessly between different banks and financial service providers. This enables consumers to use third-party apps and services to access and handle their finances while promoting competition and innovation in the banking industry.

So, why is open banking important?

For one, it promotes greater transparency and competition in the banking industry. By sharing customer data, third-party providers can offer new and innovative services that were previously unavailable. This can lead to lower costs, better products, and more personalized consumer banking experiences.

Open banking can also make it easier to manage finances. By giving third-party apps access to their banking data, consumers can more easily track their spending, control their budget, and identify opportunities to save money. This can help promote financial literacy and empower customers to make informed financial decisions.

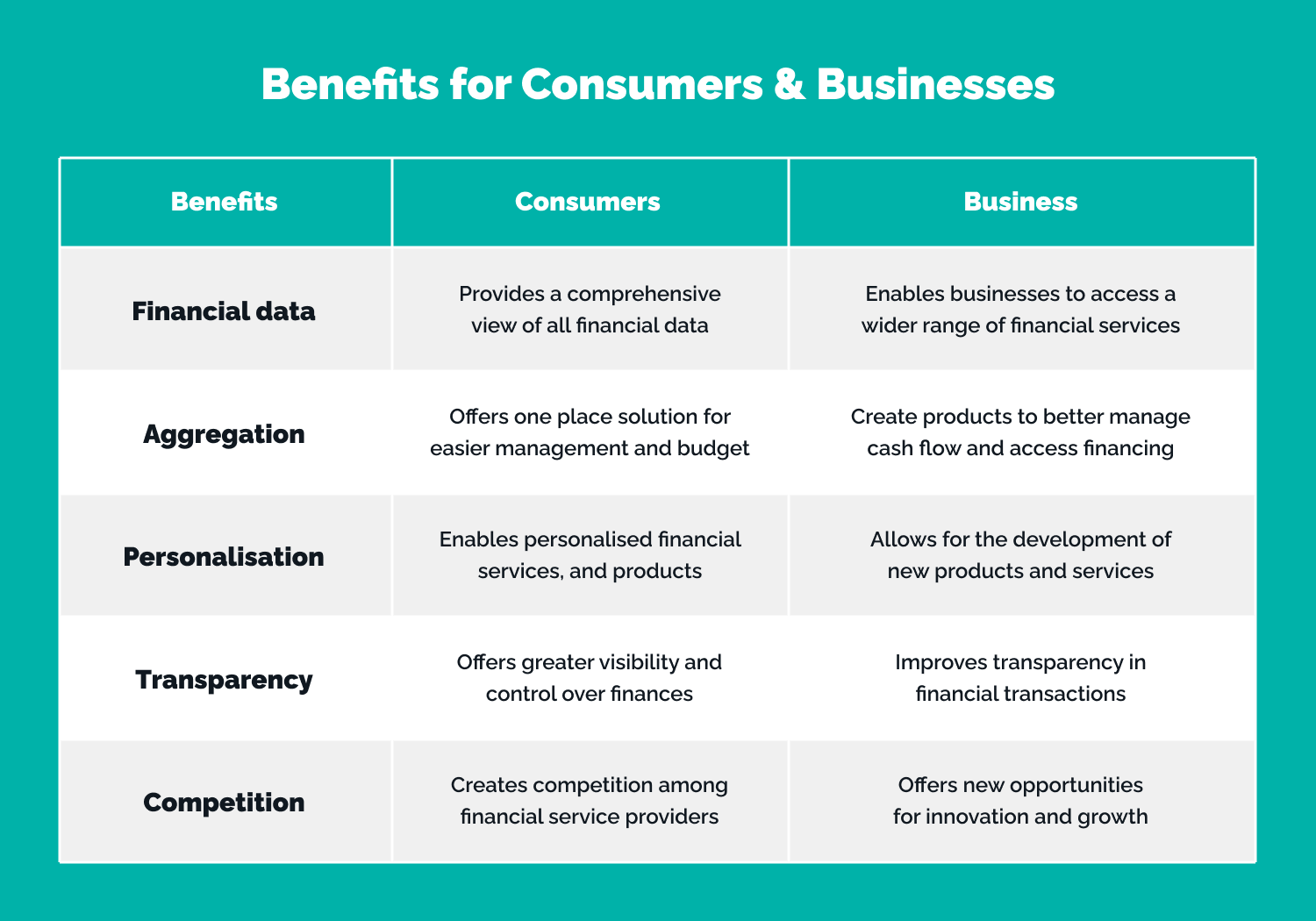

Let’s discover more benefits for customers and businesses.

Benefits for Consumers and Businesses

As a banking software development company, we cover benefits for both consumers and businesses.

Overview of The Current State of the Open Banking Industry

Many countries, including the UK and the EU, have already implemented open banking regulations. More are expected to follow in the coming years. As a result, a growing number of fintech startups and established financial institutions are building open banking solutions and services.

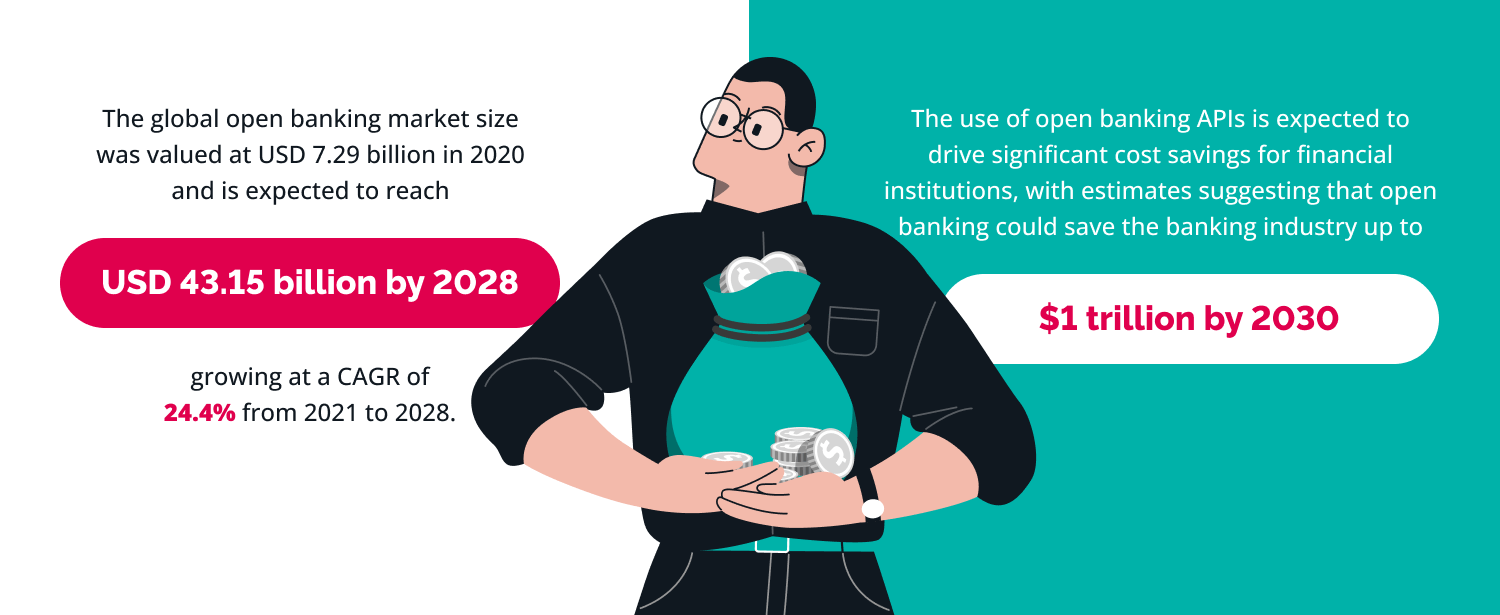

The global open banking market size was valued at USD 7.29 billion in 2020 and is expected to reach USD 43.15 billion by 2028, growing at a CAGR of 24.4% from 2021 to 2028.

We summarise a few impressive facts about the open banking movement:

- In Europe, the implementation of the PSD2 directive has driven the growth of open banking, with 78% of European banks providing open banking services in 2020.

- The UK is a leading market for open banking, with over 300 fintech companies operating in the open banking space.

- The use of open banking APIs is expected to drive significant cost savings for financial institutions, with estimates suggesting that open banking could save the banking industry up to $1 trillion by 2030

Overview of Existing Solutions in the Market and Key Trends

Open banking has been a rapidly evolving field. As such, some existing solutions in the market are now that consumers and businesses are utilising.

Some examples of existing solutions in the open banking market include:

- Payment initiation services: It enables consumers to make payments directly from their bank account to a merchant without needing a card payment. It is faster and more secure than traditional payment methods.

- Account aggregation services: These allow consumers to view and manage all their financial accounts in one place, regardless of which institution they are with.

- Personal financial management (PFM) tools: It provides personalised insights into a consumer's spending habits and financial health and can offer recommendations for how to save money or reduce debt.

- Lending platforms: These use open banking data to offer consumers and businesses access to a wider range of lending products with more competitive rates and terms.

Overall, the open banking industry is still in its early stages, but it is rapidly evolving and is expected to transform the financial services sector in the coming years. As more consumers and businesses embrace open banking, we expect to see a wide range of new solutions and services that will make managing finances easier, more convenient, and more secure than ever before.

Some key trends and innovations in the open banking industry include:

- Use of artificial intelligence (AI) and machine learning (ML) to analyze customer data and provide personalized financial services and products.

- Development of blockchain technology to enhance security, reduce fraud in open banking transactions, and implement digital wallet development service.

- Expansion of open banking beyond the financial sector to healthcare, energy, and telecom industries.

- Mobile app development services of open finance, which extends open banking principles to other financial products and services, such as insurance and pensions.

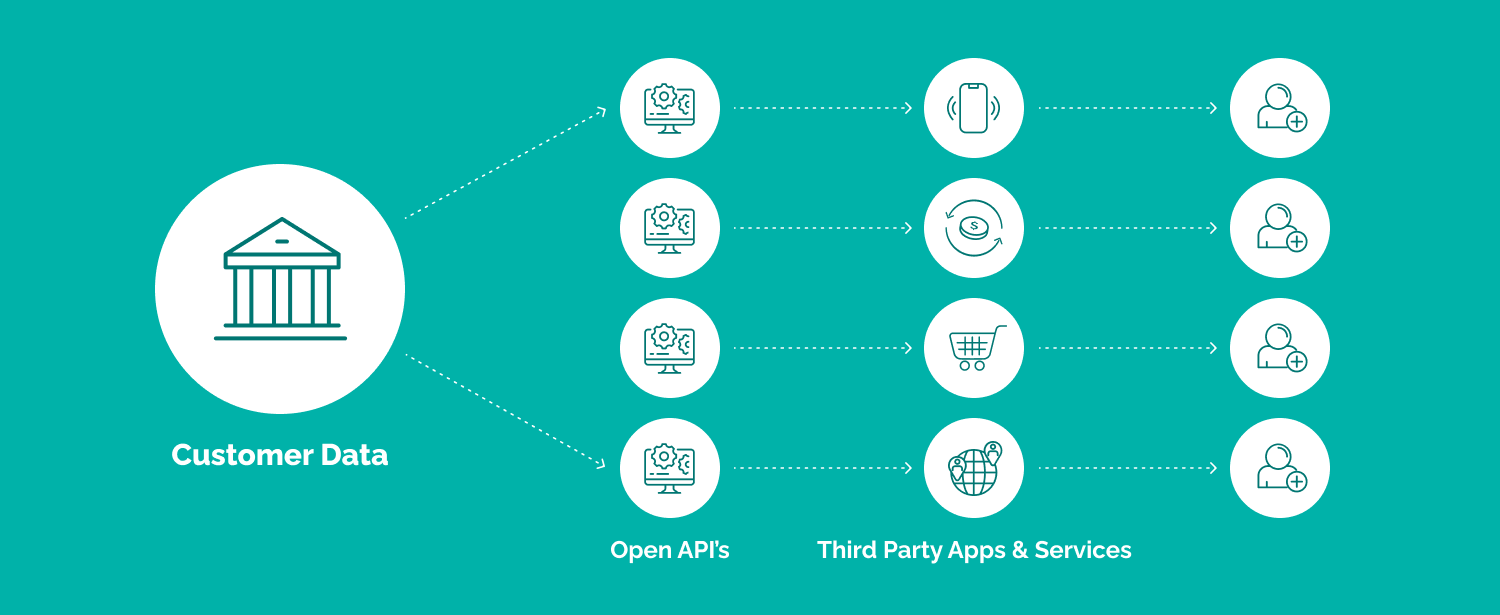

How Do Open Banking APIs Work?

Open banking APIs (Application Programming Interfaces) provide a secure way for third-party providers to access customer data and initiate transactions. APIs are a key part of the open banking framework, allowing banks to share data with third-party providers in a controlled and secure way.

Let’s look at how open banking APIs work.

Customer Authorization

For a third-party provider to access a customer's data, the customer must first give explicit consent. This is usually done through the third-party provider's application, redirecting the customer to the bank's authorization page. The customer then logs in to their bank account and authorizes the third-party provider to access their data.

Data Sharing

Once the customer consents, the bank shares the customer's data with the third-party provider through an API. The API allows the third-party provider to retrieve the necessary data, such as transaction history and account balance, in a secure and standardized way.

Transaction Initiation

In addition to accessing customer data, open banking APIs allow third-party providers to initiate transactions. For example, a third-party provider could use an API to initiate payment directly from the customer's bank account without the need for the customer to log in to their online banking.

Security

Open banking APIs use various security measures to keep customer data safe. This includes encryption, two-factor authentication, and access controls to limit the data that third-party providers can access.

Overall, open banking APIs provide a way for third-party providers to access customer data and initiate transactions in a secure and standardized way. This allows for greater competition and innovation in the banking industry and gives customers greater control over their data and services.

Make sure building 100% secure app

Learn moreIntegrations with Open Banking

Successful open banking implementations include Starling Bank, which has built innovative banking products and services using open banking APIs, such as its Marketplace for third-party products and services. Another example is Revolut, which has leveraged open banking APIs to provide users with personalized insights and recommendations for managing their finances.

Also, integrating with open banking tools requires compliance with specific security regulations to protect sensitive financial information. Open banking as API security, data protection, and customer authentication is regulated by

- the Payment Services Directive 2 (PSD2) in Europe

- the Financial Conduct Authority (FCA) in the UK

Top Open Banking Apps of 2023

Open banking is rapidly changing the financial services industry. As we move into 2023, many open banking apps are poised to make a significant impact. From established players to promising startups, the following is open banking apps review, covering a range of categories:

Plaid

Plaid is a fintech company that provides a suite of APIs for financial institutions and fintech companies. With connections to over 11,000 financial institutions in the US, Plaid allows businesses to securely access customer data and build innovative financial services and products. Its key features include transaction data, account balances, and authentication. Its products enable developers to build applications connecting users' bank accounts, credit cards, and other financial accounts. Companies like Venmo, Coinbase, and Robinhood use Plaid for innovative technology solutions. In 2020, Plaid was acquired by Visa for $5.3 billion.

Tink

A Swedish-based open banking platform that connects financial institutions to over 3,400 banks across Europe. Its APIs enable businesses to access account data, initiate payments, and verify customer identity, among other features. Its platform provided account aggregation, payment initiation, and personal finance management tools. Tink has partnered with major financial institutions such as PayPal and BNP Paribas and has a strong market position in the European open banking landscape. In 2021, Tink was acquired by Visa for $2.15 billion.

Yapily

A London-based open banking platform that provides APIs for businesses to access banking data across the UK, Europe, and beyond. Its platform enables businesses to access bank account data, initiate payments, and verify account ownership, all through a single API. Yapily currently serves over 2,000 businesses across Europe and has raised over $69 million in funding.

Coconut

Coconut, which recently transformed a neobank into a banking hub, giving customers more options, is an intriguing example of an open banking application. To assist the self-employed community, a freelance accounting companion in the form of an app has been developed. Sole proprietors can manage their income, claim expenses, and determine how much tax they owe thanks to the connection to their bank accounts. Even though it seems easy, having Coconut organize accounting procedures allows them to focus more on its work.

Basiq

Basiq is an open banking API provider allowing businesses to access and analyze financial data from banks and institutions. It has processed over 2 billion transactions and analyzed data from over 100 financial institutions across Australia, New Zealand, and Southeast Asia.

Basiq's platform enables businesses to create new financial products and services that offer customers personalized financial advice and services in real-time. By leveraging Basiq's APIs, businesses can offer value and convenience to customers and drive revenue growth.

Bud

A UK-based personal financial management app allows users to aggregate all their financial accounts in one place, providing personalized insights and recommendations. The app uses open banking APIs to securely connect to users' accounts, offering personalized insights and recommendations for how to save money and optimize spending. Bud's machine learning algorithms analyze users' financial data to provide personalized product recommendations. Users appreciate the app's ability to help them save money and find better financial products.

Mint

September 2007 saw the launch of Over 40,000 users joining Mint in its first two weeks, and it today has more than 15 million members. Mint is a popular personal finance app that allows users to link their bank accounts, credit cards, and other financial accounts in one place.

To help their customers stay on top of their accounts, invoices, and subscriptions, Mint compiles all user accounts into a single dashboard. Mint aids in budgeting, tracking costs, setting savings objectives, keeping track of credit scores, and other tasks. The user's financial information and transactions are automatically synchronised after the accounts have been downloaded and linked.

Cleo

The AI/ML-powered Cleo app connects to bank accounts, monitors and categorizes transactions, and provides proactive financial advice and information. Simply texting "budget" or "save" to the chatbot will activate choices for creating a budget or saving goals. But its best "hyping/roasting" mode is its most unique feature. To encourage the user, Cleo praises them when they spend less or "tough love" when they go over budget.

In 2020, Cleo had 4 million enrolled users, and the company reported a 400% increase in income during the previous 12 months. Barnaby Hussey-Yeo, a data scientist, founded this fintech business in January 2016 and has raised $44 million in Series B funding.

Digit

An app called Digit invests and saves money for users automatically. After being linked to a bank account, the app's AI examines the account balance, recurring bills, income, and spending patterns. Digit helps users save the ideal quantity of personal funds by automatically transferring money from their checking account to Digit accounts when they can.

A post-money valuation of $277.5 million was given to the 2013-founded company, which saved users $5 billion. Digit receives revenue via subscription fees, commissions for referrals, fees for withdrawals, and interest on the money held in user bank accounts.

Currensea

The first travel money card in the UK that supports all currencies and is directly connected to a user's bank account is called Currensea. The business was established in 2018. In just over two weeks, the Seedrs crowdfunding effort raised 102% more than its £800,000 funding goal. The initiative went on to win a £1.5 million prize fund run.

The card enables users to avoid up to 85% of transaction and currency rate expenses. Users don't need to establish a new account because the card is an extension of their present one.

Synapse

Synapse is a platform that provides APIs for banking services such as account creation, KYC verification, and transaction processing. It aims to simplify banking operations by offering a single point of integration and customization of various banking products. Synapse has raised $175 million in funding, and its clients include leading fintech such as Robinhood and Betterment.

Figo

Figo was a German-based startup that aimed to offer an open banking platform to businesses and consumers. Its platform provided account aggregation, payment initiation, and personal finance management tools. It raised over €12 million in funding but could not gain significant market share. In 2020, Figo filed for bankruptcy after being unable to secure additional funding.

The company's failure has been attributed to a lack of focus and poor execution, as well as a crowded market with many competitors.

Lessons Learned from Failed Experience

While some startups have failed, many lessons can be learned from their experiences. Failed startups highlight new players' challenges in the highly regulated and competitive banking industry.

Some key lessons that can be learned from their experiences include:

- Regulatory compliance is critical: Startups must be prepared to navigate complex regulations and obtain the necessary licenses to operate in the financial services industry.

- Customer acquisition is difficult: Building a strong customer base takes time and resources and requires a well-defined value proposition that meets a specific customer need.

- Funding does not guarantee success: While funding can provide a startup with the resources to build and scale its product, it does not guarantee success in the market. Startups must demonstrate traction and a path to profitability to attract continued investment.

Wrapping up

Open banking apps have the potential to revolutionize the financial services industry. By leveraging the power of open APIs, these apps offer users a new level of convenience and control over their financial lives. By enabling seamless financial data integration across various institutions, open banking apps offer many benefits, such as increased transparency, improved access to financial products, and personalised financial advice.

Nonetheless, the list of top open banking apps to watch in 2023 showcases a wide range of innovative solutions that have the potential to transform the way consumers and companies manage their finances. Each app offers unique features and strengths that distinguish it from its competitors, and they are all well-positioned in the highly competitive open banking market.

FAQs

-

What are open banking apps?

Open banking apps are third-party applications that use the open banking infrastructure to offer consumers various financial services. They typically connect to a user's bank account and use their transaction data to offer budgeting, savings, investment, and loan management services.

-

Are open banking apps safe?

Open banking apps must adhere to strict security standards to protect user data. They typically use encryption and other security measures to ensure that sensitive information is not compromised. However, users should always read the app's terms and conditions and privacy policy before granting access to their financial data.

-

How do open banking apps work?

Open banking apps use APIs to access a user's financial data and use it to provide financial services. The user grants permission to the app to access their data, and the app can then securely connect to their bank account and retrieve the necessary information.

-

What are the benefits of using open banking apps?

Open banking apps offer personalised financial advice, streamlined budgeting and savings tools, and access financial products and services from different providers. They can also help users make more informed financial decisions by providing insights into their spending and saving habits.

linkedin

linkedin

facebook

facebook

twitter

twitter