TechMagic Academy

TechMagic AcademyThe Hottest Fintech Trends For 2026

Last updated:11 January 2026

The traditional financial institutions will likely not be the same anymore. Looking forward, it’s expected that we will see further changes in the way of living and interactions between people.

About 90% of people in the USA use fintech services now. Global quarantines and lockdowns have made digital financial processes more customer-focused. It stimulates fintech companies to keep up with the times and actively adopt the latest emerging technologies, to provide the expected level of services and keep a high satisfaction rate.

The fintech market is estimated at $698.48 billion in 2030, while in 2020, it was $110.57 billion. Startups and established organizations are keeping up with new technologies and the pace of change and updating their operations and amassing enough technical skills and tools.

If you don't scale - you fail. But you also need to ensure the relevance of the scalable solution — this is why fintech companies might consider adopting new fintech industry trends 2026 to gain an advantage over your competitors.

We researched the finance industry to find out how exactly fintech companies will approach increasing their efficiency. From BNPL to cryptocurrencies, how the payment world digitalizes and revolutionizes, and what place fintech innovation would have in recent years - all these and more details of fintech trends 2026 we have covered in this blog post.Without further ado, let's get to the top trends in fintech!

Embedded finance

According to an analysis by Dealroom, the market for embedded finance solutions is expected to reach $7.2 trillion by 2030, surpassing the combined value of fintech startups and the top 30 global banks and insurance companies.

Embedded finance refers to the seamless integration of financial products and services into non-financial platforms or applications, making financial functionalities an integral part of everyday experiences. This trend is breaking down silos between finance and other industries, offering users convenient access to financial services without the need to engage with standalone banking or financial applications. For different fintech companies this enhances accessibility for customers, allowing them to use digital wallets or other fintech-based payment methods during online purchases, including online savings accounts.

Examples of fintech trends include interest-free loans at online checkout, user-friendly one-click payment apps, and the introduction of branded checking accounts and debit cards for core users.

Open banking

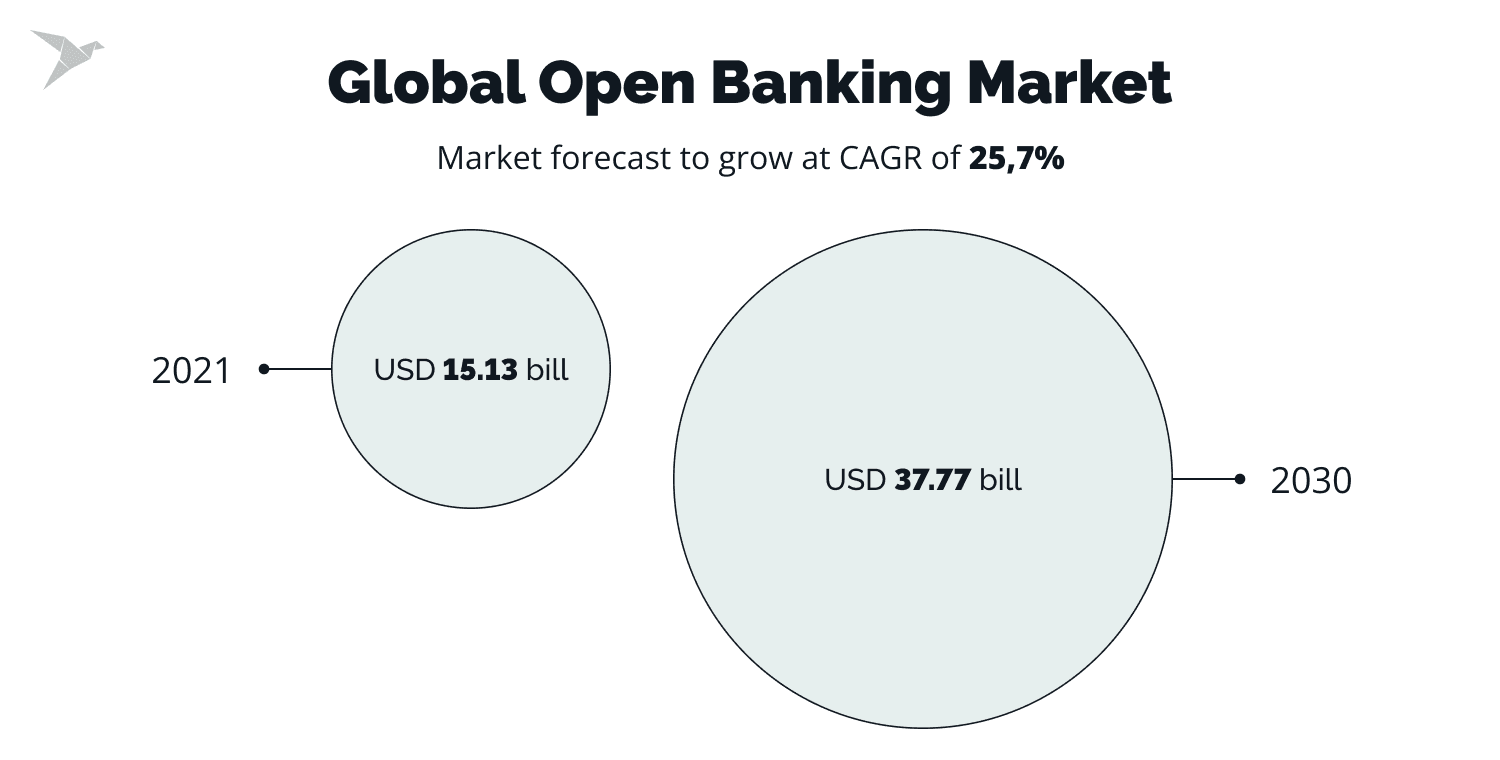

In 2024, 63.8 million people will use open banking, predicts Statista. In comparison to 2020, this is almost five times more.

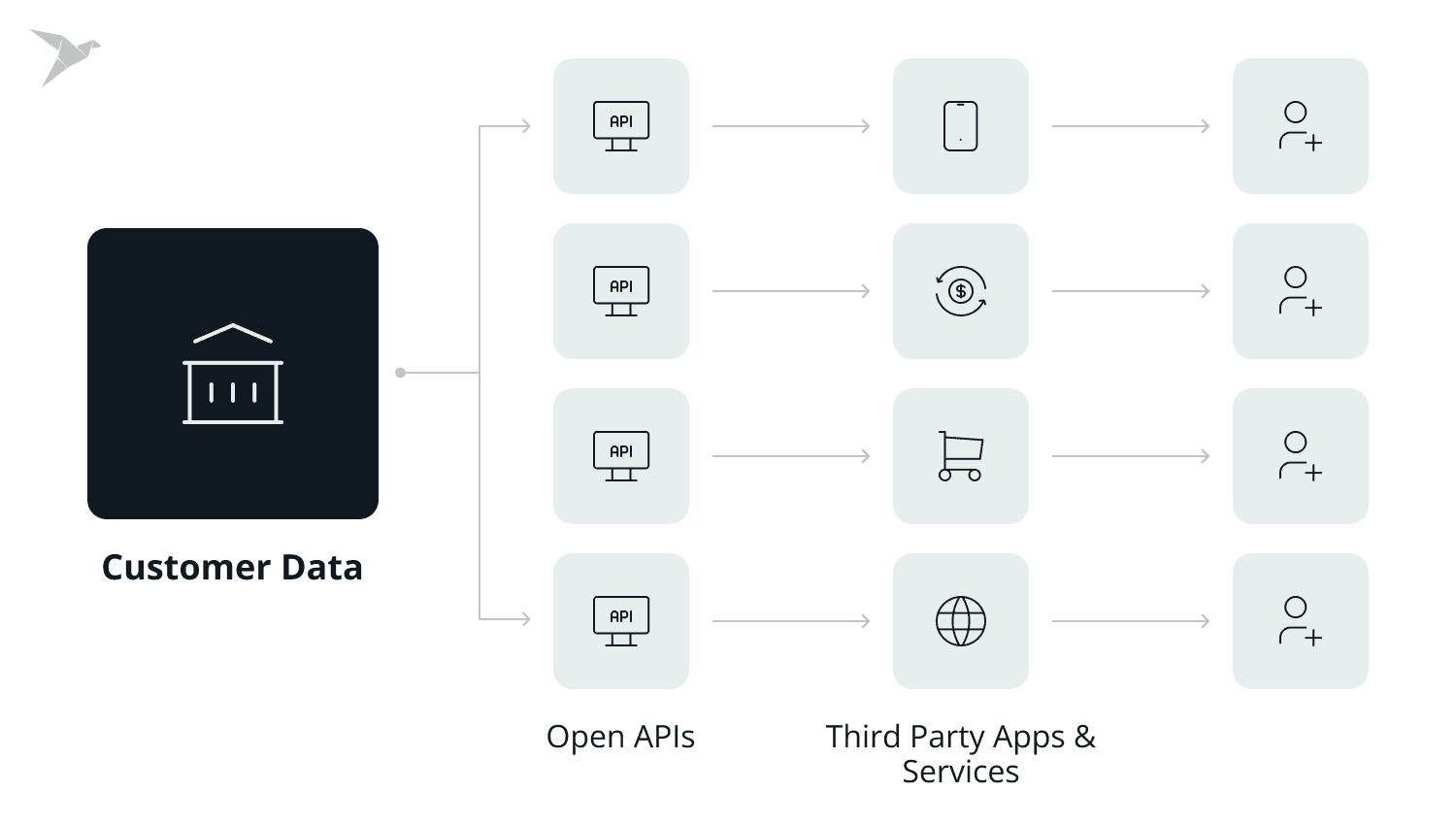

Open banking focuses on controlled financial information exchange. Account holders can accept procedures for safely sharing their financial data with nontraditional financial institutions. Accessible APIs enable third-party suppliers to access the clients' financial data. Many fintech startups and businesses that offer budgeting, expense tracking, financial planning, lending, and other services use open banking prospects.

According to McKinsey, just 10% of open banking's promise is realised. This is financial technology sector still shows promise. Users are slowly beginning to understand the advantages of working with open data since information interchange promotes scholarly investigation, software advancement, and enhancement of financial services.

Open banking and using APIs to securely share information will simplify, accelerate and drive greater transparency and "pull through" in the purchase or financing of products, the movement of money and other transactions. As a result, consumers should see lower loan rates and more frequently hear "yes" when submitting applications as lenders compete and apply richer data sets to their credit models. - Greg Mitchell, First Tech Federal Credit Union

For instance, a devoted customer might decide not to switch financial institutions because they are happy with the dependability and stability of their bank. However, the bank is quite conservative, and many of the digital services offered by rivals have not yet been adopted.

- The client wishes to link analytics tools to financial data to analyze customer behavior spending and spending patterns.

- The bank likes to retain dependable clients.

- As a result, it gives the owner's data to a third party that deals with analytics with an API. It is accomplished via the API.

Thanks to open banking apps, the account holder benefits from regular reports on the balance, expenses, and savings.

The bank can give insurance companies, retailers, and other businesses access to the client's finances through open APIs. Before implementing insurance, providing a loan, or allowing payment by installments, they must confirm the client's solvency in banking industry. With the help of open banking, users can now pay for goods and services online quickly and easily, receive a loan quickly, and pay for services with a single swipe.

Neobanking

The pandemic has taught us that we can do anything from home, and the financial banking industry has also taken it seriously. FinTech has contributed to the growth of neo-banks. Neo banks as a fintech trends resemble traditional banks but do not have any physical locations.

- Thus, Neo banks are equipped with all the features of a traditional bank branch. Instead of traditional bank branch models, many new FinTech businesses are focused solely on the Neo banking concept. It is a win-win approach for companies and customers due to the cost reduction and ease of access.

- Neobanks are a type of fintech company that exists to lower the cost of banking services. Compared to larger banks, they often provide fewer service categories but concentrate on these categories to raise the quality of those services.

In the year 2021 alone, neobanks boasted a customer base exceeding 145 million globally. Projections indicate a surge, with expectations reaching a 360 million customers by the year 2026. At a period when remote work was essential for many businesses, instant transfers, quick registration, and IBAN and ACH accounts enabled completely online banking access is a significant advantage.

Statista report shows that 48% of respondents prefer Chime. Over 13 million people access personal banking with Chime, one of the biggest neobanks in the US. With their mobile banking app, Chime makes access to cash for any direct deposits set up to your bank account two days earlier.

Chime offers essential banking services, alternatives for debit and credit cards, and a user-friendly interface. Fintech companies can grow your credit and save money for the future while using Chime to access necessary banking features without paying fees.

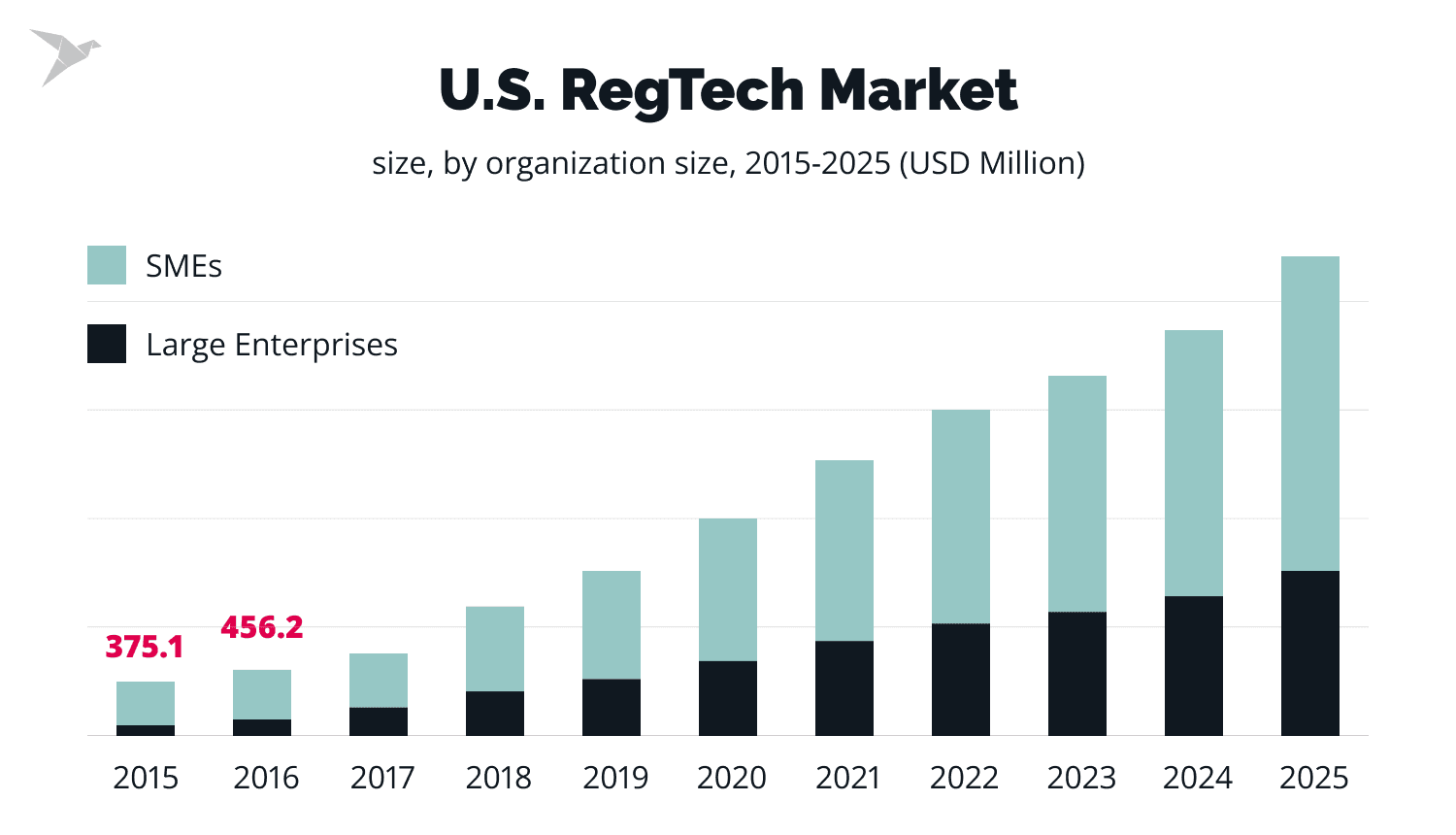

RegTech (Regulatory Technology)

Financial institution operations are governed by laws, standard practices, and regulations that one must be aware of and adhere to. Businesses must maintain accounting records, tax reports, income reports, and customer reports. According to the timetable, they deliver the required paperwork to regulatory establishments. They verify the accuracy of the data and the activity's legality. Regulatory technology can help in this situation.

RegTech is a type of technology used to monitor regulatory compliance. Regulatory technology identifies problems that don't follow the rules and makes them work with the system. Specialised software automates monotonous procedures, keeps an eye on data security, and alerts users and bank workers to fraud.

Millions of dollars are imposed as penalties for non-compliance. For instance, the Bank of America Corporation previously had to pay $42 million to New York State for providing clients only a cursory explanation of how their share orders were handled.

RegTech makes it simpler for organizations to communicate with their regulatory authorities so that data may be sent without interruption, compliance is monitored (for example, by adhering to PCI compliance rules), and financial crimes are tracked.

Learn about our expertise in the industry and what we have to offer

Green Banking

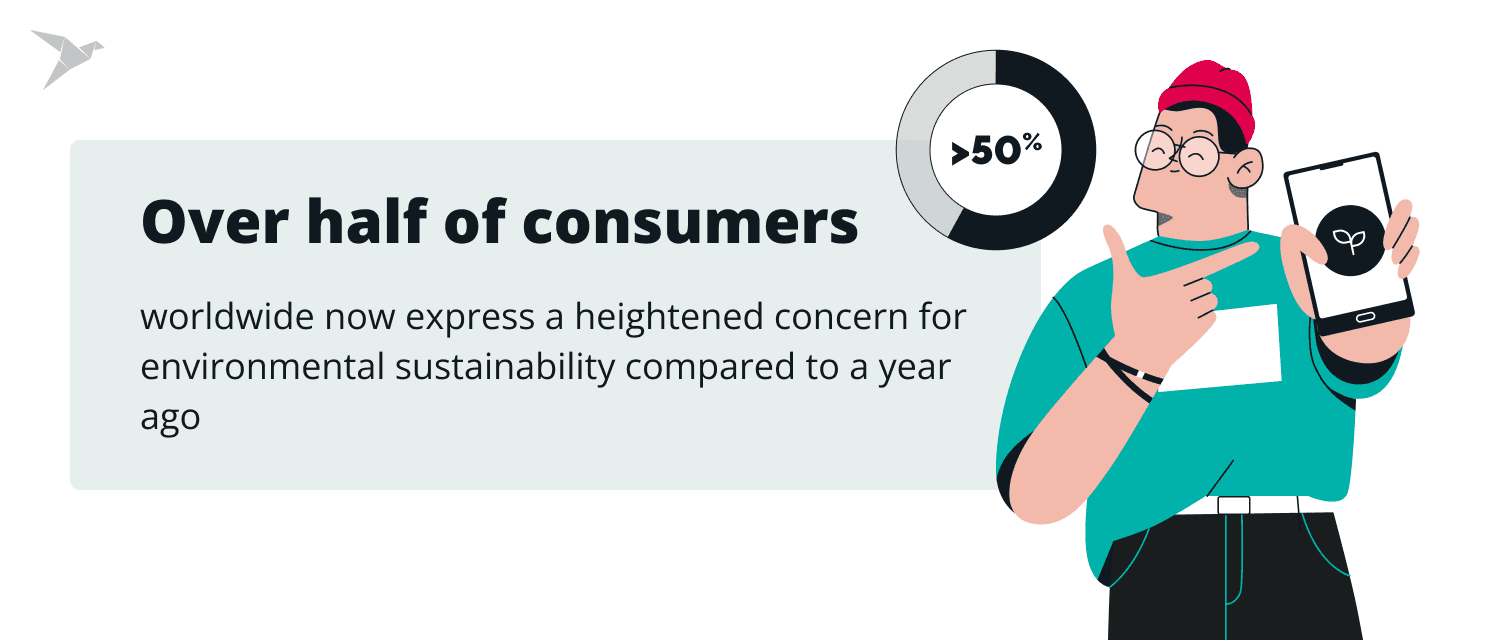

Over half of consumers worldwide now express a heightened concern for environmental sustainability compared to a year ago. Sustainability has become a significant factor among fintech trends in how organizations are evaluated by investors, consumers, and fellow entities.

Certain fintech entities and banks are already forging ahead in sustainability, with numerous Neobanks and payment providers committing to ESG (Environmental, Social, and Governance) disclosure. These industry players are actively developing environmentally conscious financial products and services.

Digital payments exhibit a more eco-friendly profile than traditional cash and credit cards. These fintech companies are undertaking measures to curtail their ecological footprint. Some banks, for instance, are pledging to achieve carbon neutrality and minimize waste generation.

As awareness regarding the significance of sustainability grows among consumers, there is a heightened likelihood between fintech trends of them favoring financial institutions that demonstrate unwavering commitment to social and environmental responsibility.

Artificial Intelligence and Machine Learning

The worldwide market for AI in fintech is a growing industry expected to reach an astounding $26.67 billion by 2026 while maintaining a CAGR of 23.17% from 2021 to 2026. More than 90% of international fintech businesses already extensively depend on AI and machine learning.

By gathering and processing data about customers' cash accounts, credit accounts, and investments, AI enables financial institutions to monitor their client's financial health and offer them more relevant and individualized services. ML models examine various factors to identify potential fraudsters, resulting in a significant 20% reduction in the workload required for investigations.

Companies can use cognitive automation, engagement, data analysis, and insights capacities to improve smart banking services.

AI can:

- manage client data,

- offer suggestions on management strategies,

- catch human errors,

- and control banking quality.

Artificial Intelligence can also interact with clients directly via chatbots and self-learning apps. AI-powered chatbots and digital assistants can generate context-aware content, enabling them to assist users in tasks such as selecting investment opportunities and navigating complex financial decisions. Moreover, modern chatbots are also latest fintech trends that can retain the context of previous interactions with users, allowing for more meaningful and useful responses based on past inputs.

UBS Group, one of the world's most significant financial holdings, partnered with a Singapore-based fintech company that uses AI for banking assistants. UBS Group developed a premium service in financial sector that allows VIP clients to get intelligent insights and forecasts about their revenue and expenses.

To make this innovation happen, UBS organized Innovation Challenge, where more than 80 teams competed for a $40,000 reward and a contract from the company. The final app analyses the data of UBS clients and delivers insights into their laptops, smartphones, and iPads. Companies seeking to build similar AI-powered products turn to specialized FinTech development services to accelerate delivery and ensure compliance.

AI provides many opportunities, and we will not dwell on them in detail now, but we want to highlight Robo-advisors due to their rapidly gaining popularity.

Robo-advisors

With the development of artificial intelligence, many investors may now benefit from computerized personalized financial advice guidance. Robo-advisors and personal financial managers use AI ideas to show investors the best ways to spend their money.

These sorts of applications are a disruptive force in the industry and tremendously profitable.

Based on AI data analysis algorithms, Robo-advisers can:

- analyze massive volumes of data,

- adjust to a changing environment quicker than human advisors,

- present investors with the best investment alternatives to achieve their objectives.

Robotic process automation are particularly well-liked among rookie investors who lack access to traditional counseling since alternative investing instruments have considerably decreased the entrance load for investors and allowed nearly anybody to generate money, even with little cash.

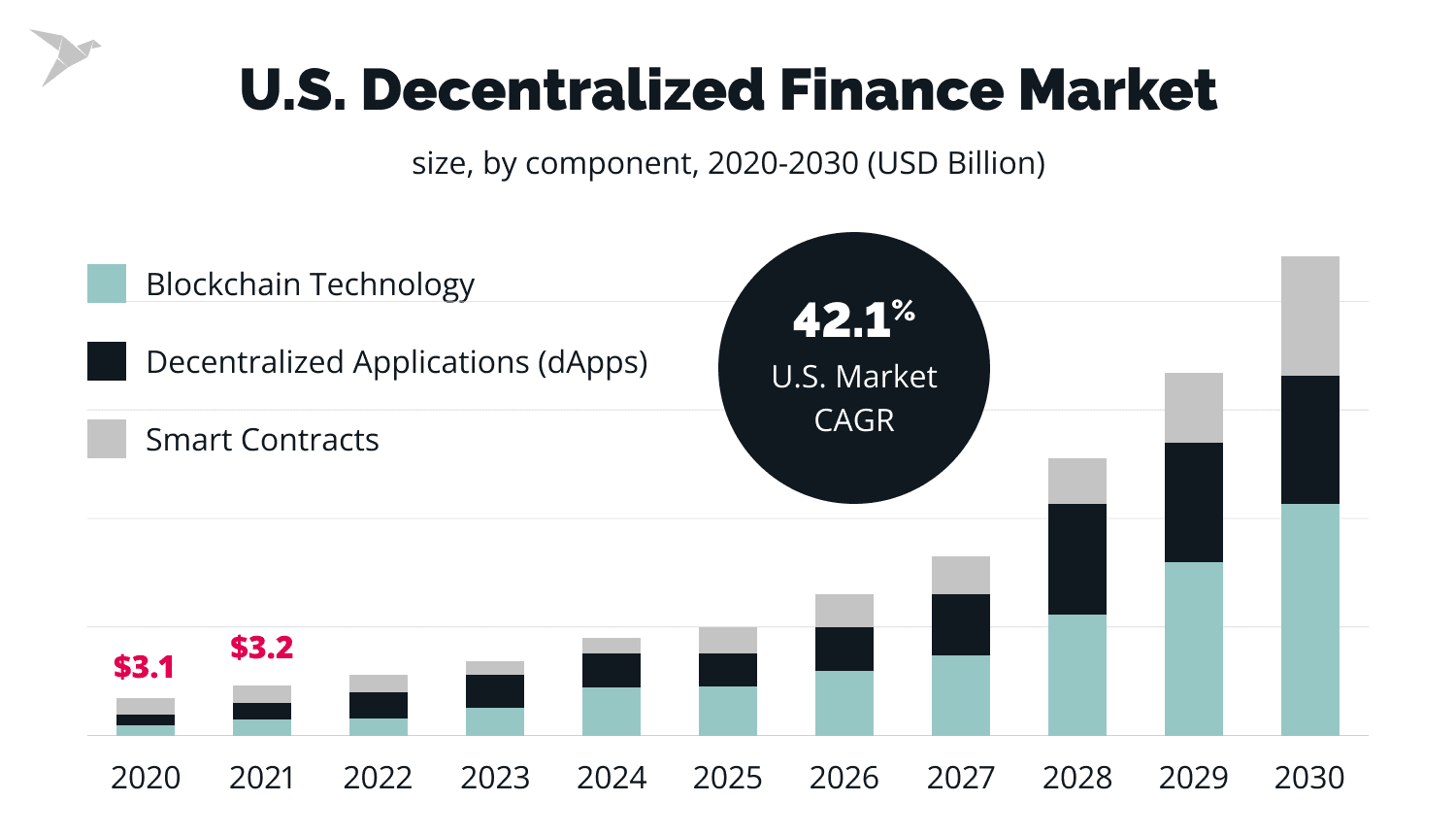

Decentralised Finance (DeFi)

Though connected with the cryptocurrency market and alternative financial instruments, decentralised finance is a new growing fintech trend 2024.

DeFi is represented by various decentralised financial products that function without a central authority, such as:

- loans,

- exchanges,

- payment applications,

- etc.

DeFi uses self-executing smart contracts for all management and is open source, giving users more confidence. It now makes it easier for multiple blockchains to interact with one another, elevating the cryptocurrency industry to a new level open to a broader audience. On the market, there are a lot of DeFi initiatives that can compete with centralised financial solutions.

Blockchain

The global blockchain market will grow 143 times before 2030 with a total volume of $1,5 trillion. The main financial services, including Visa, Mastercard and PayPal, have started to use cryptographic assets and allow others to make cryptographic payments.

The procedure of sending money internationally is currently time-consuming and costly. However, blockchain technology seeks to overcome these challenges with greater speed and security for foreign payments and reduced prices.

Blockchain technology is sometimes called a "distributed database" or "electronic ledger." Each transaction is documented in a unique block connected to the network's earlier blocks. The participants may all access it.

Only with the consent of more than 50% of the participants is a transaction legitimate. Because each block has a different hash and verification is required to complete each transaction, it is difficult to "open" such a decentralised network.

Blockchain's digital ledger technology addresses many issues plaguing the financial industry today, especially security and efficiency. In fact, it subverts institutions in a way that makes today's financial industry look archaic. - Jaclyn Foroughi, Brazen Impact

Blockchain RBC customers can get additional decentralised services for a certain number of loyalty points. IBM World Wire, a blockchain system launched by IBM, allows cross-border payments worldwide, including in African countries with poorly developed local banking solutions.

Cryptocurrency

45% of customers already use cryptocurrencies for conducting international financial transfers, and more than half (52%) believe it to be a "legitimate option."

The value of these assets is rising due to the widespread adoption of cryptocurrencies by businesses worldwide. For instance, one of the biggest payment services in the world became cryptocurrency-friendly when PayPal announced support for the native transfer of cryptocurrencies between PayPal and other wallets and exchanges in June 2022.

There will be more mainstream adoption of cryptocurrency and other digital assets tied to the blockchain. Expect regulation and/or legislation to create "rules of the road" that financial institutions and investors can follow. Over time, crypto can allow faster transactions and bring more underserved groups into the financial system. - Paul Davis, Strategic Resource Management

However, the market now experiences “crypto winter” pitfalls that pose new long-term opportunities like improving inefficiencies like cross-border payment.

Smart contract

Smart contracts are a remarkable FinTech development with wide-ranging applications in the embedded financial services sectors. It manages and governs the execution of agreements that are made virtually between a buyer and a seller. Since the agreement is signed virtually using cryptographic keys, virtual transactions no longer require attorneys or paper papers.

In finance, smart contracts may be used to automate contracts without the involvement of a third party like a bank or loan officer. It implies that buyers and sellers can safely connect with a legal agreement without involving banks.

Future standardization of smart contracts might be enabled through DeFi fintech apps. Consider that you require a mortgage. You can get a loan based on a smart contract instead of going to a bank and getting the money in a few minutes or less.

Stablecoins

Stablecoins are promising fintech trends, digital currencies designed to maintain stability by pegging their value to an underlying reserve, often a fiat currency like the U.S. dollar or a commodity like gold. This stability addresses a significant challenge traditional cryptocurrencies face—volatility—and brings several important aspects to the forefront of the fintech industry.

The stability provided by stablecoins bridges the gap between the crypto world and traditional financial systems. Stablecoins streamline cross-border transactions by providing a secure and stable medium of exchange.

While initiatives of this magnitude are currently within the purview of governments, influential banks, and established cryptocurrency exchanges, the rising prominence of stablecoins suggests potential opportunities for broader adoption.

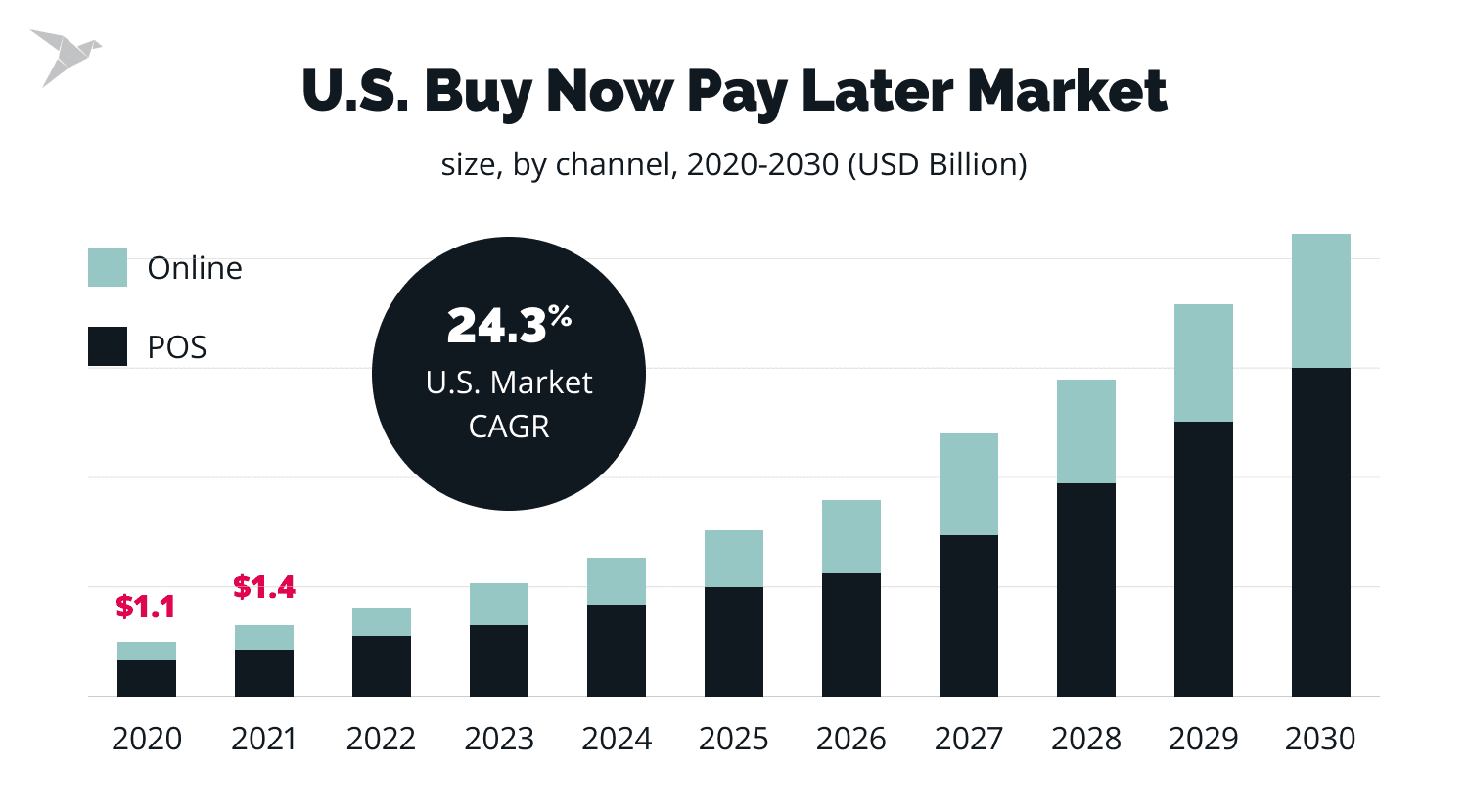

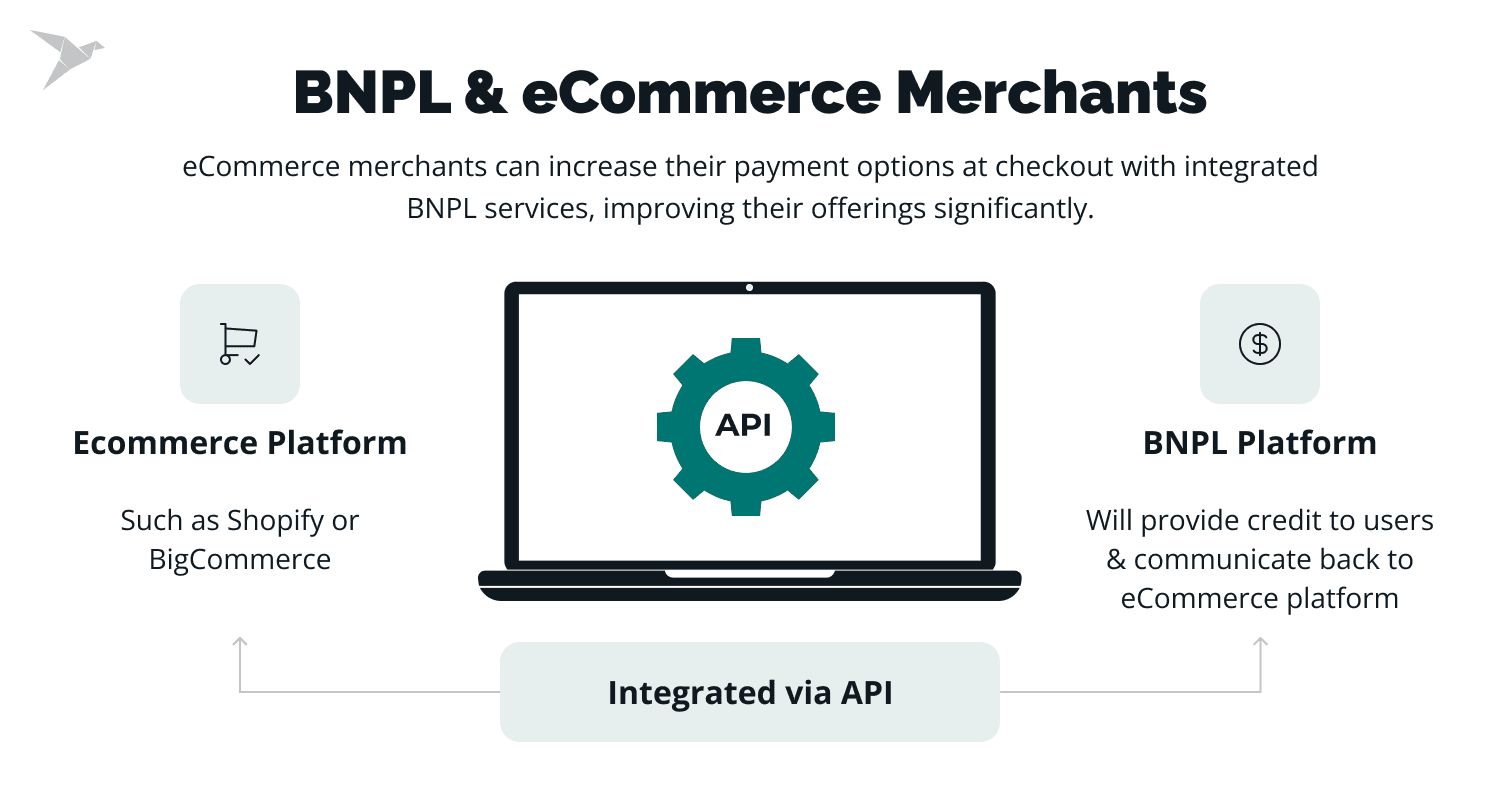

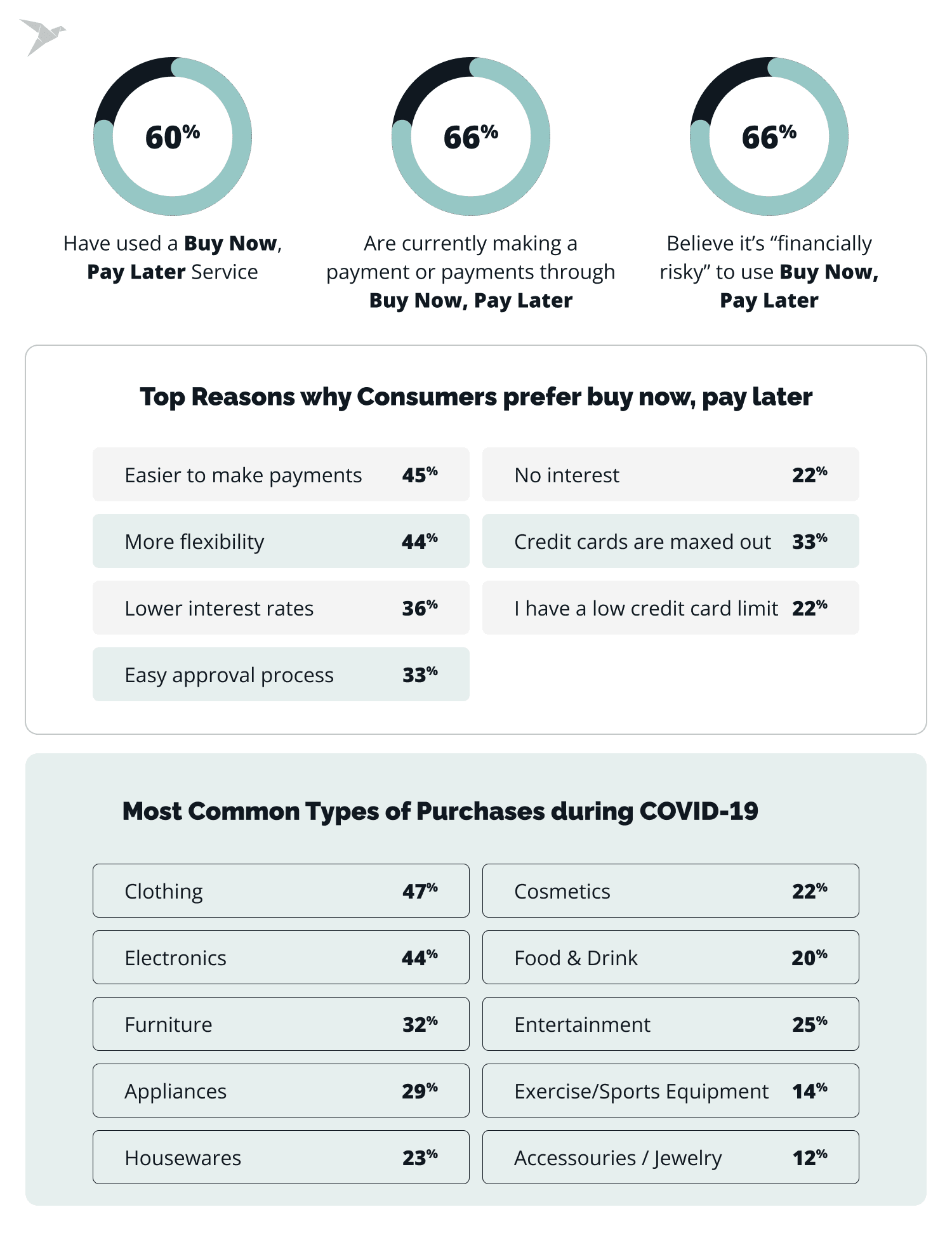

BNPL (Buy Now Pay Later)

The BNPL option is expected to be used in deals worth $576 billion worldwide by 2026, up from just $120 billion in 2021.

The BNPL boom is something you should pay attention to if you operate in a field that includes payments in any way (whether B2C or B2B).

Buy Now, Pay Later is a type of short-term financing that allows for the future payment of goods or services. This frequently functions without interest, making it a well-liked kind of funding. Customers who use point-of-sale instalment loans make a down payment on an item and then pay the remaining balance later.

For instance, Amazon and Affirm are working to implement BNPL by dividing payments for purchases of $50 or more into smaller monthly instalments.

One of the most well-known BNPL systems is provided by the multinational financial business PayPal. Customers can use this service to split a maximum payment of $1,509 into four equal payments payable every two weeks.

At the time of purchase, the initial payment is made. Pay does not charge late fees and does not file credit bureau reports.

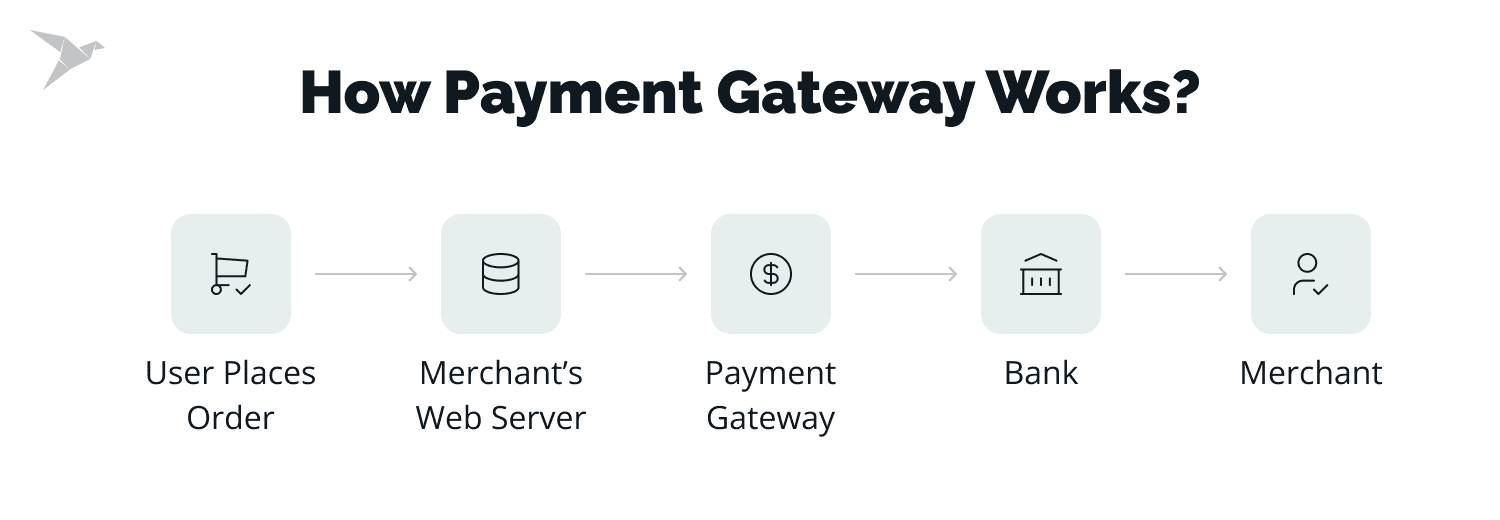

Payment Gateways

For online purchases, more than 55% of US customers use credit cards and more than 52% use debit cards. Building a payment gateway is required for all of these transactions. Payment gateways establish a connection between clients and retailers to facilitate efficient bank-to-bank transactions.

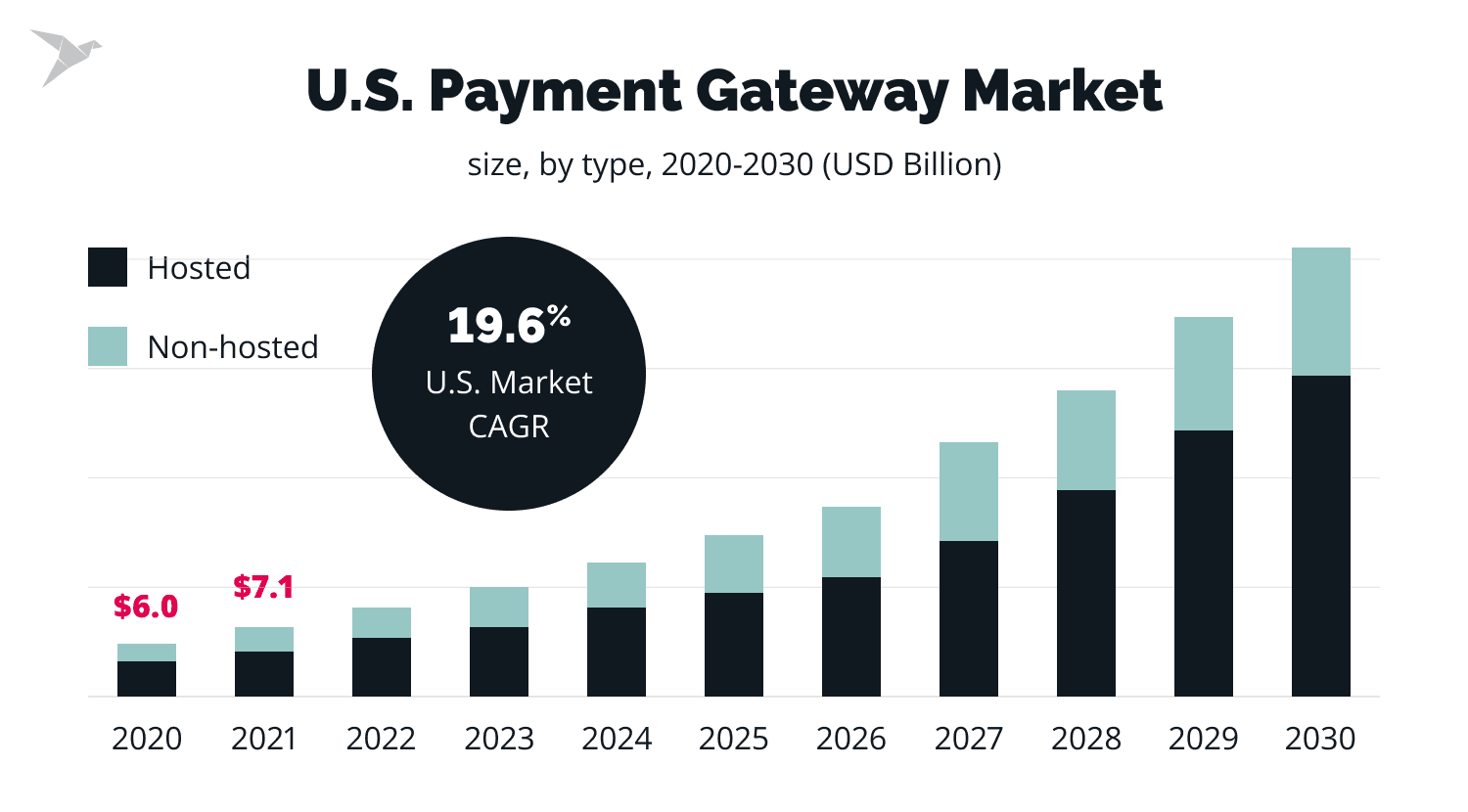

The market for payment gateways is rapidly expanding due to the volume of transactions and the number of merchants constantly rising. It is currently valued at $17.2 billion, but by 2026, it will be worth $42.9 billion.

One tool doesn't offer some payment method, another doesn't provide cross-border support, or one's commission is too high — and business owners need to combine many services to compensate for these issues. In 2024, the simplicity of the payment stack will be a priority among trends in fintech.

Payoneer is an excellent example of a universal payment system available in more than 200 countries. It allows the fintech company to partner with multiple banks and businesses and establishes a powerful global presence.

Many businesses that work with international communities list Payoneer as their primary payment method like Airbnb, Univera, and others. This trend fintech declares fintech payment companies should focus on getting dedicated international partners and connecting to marketplaces.

Banking as a service is changing the way we manage our business. Integrating an automated payables program with your online banking platform could save you thousands of dollars in time, energy and treasure. Integrating payments with payables is essential to creating efficiencies for your customer and vendor management. - Anthony Holder, C&H Financial Services, Inc.

Biometric Authentication

Business Performance Innovation Network reports that financial companies that rely on passwords rather than easy-to-use biometric identity verification procedures will lose clients. Especially when gaining access to money and other financial information, 81 per cent of customers actively seek out firms that offer a rapid identity verification or authentication experience. Companies that use this level of security have raised the bar, and fintech businesses are paying attention.

The safety of bank accounts is seen as an essential concern by 93% of consumers, making FinTech a priority sector for biometric authentication technologies. The worldwide biometrics market will increase from $42.9 billion in 2022 to $68.6 billion in 2025, according to Statista.

Improving the efficiency of a fintech solution is directly connected to investing in its safety. A fintech solution should guarantee safe data storage and processing and withstand cyberattacks. These are not new trends in fintech, but with the growth of digital banking, security measures have become increasingly more relevant.

Cybersecurity experts believe that biometric authentication is safer than traditional passwords and PINs. According to Dr Thirimachos Bourlai of West Virginia University, biometrics can effectively guard against theft or fraud regarding personal information. Unique fingerprints and voices cannot be faked.

Apps and services that demand a high level of security, such as those used by banks and other financial institutions, are likely to include biometric authentication more frequently in the future. And as the market expands, we'll observe additional technological advancements, including adding new biometric authentication methods such as voice recognition (which will act like PIN codes). - Neil Anders, Trusted Rate, Inc.

Users, despite having several passwords think biometric identification is the best method to confirm their identity. They need to remember one new password yearly; they do not need to learn letter and numerical combinations. Confidential information will still be secure even if your laptop or smartphone is taken.

A British firm, IDcheck provides biometric verification for financial services. The business uses proprietary face recognition, liveness check, and motion analysis technologies to identity papers.

Additionally, it recognises con artists who hide the camera with objects and photographs, preventing verification. After giving client reports, IDcheck deletes all biometric information, removing privacy issues in the case of cybercrime. The biometric screening offered by IDcheck is used, among other things, for document and ID and know-your-customer (KYC) verification.

Customer-focused

Voice payments

According to Statista, there were 8.4 billion more voice assistants than humans on the planet in 2025. By integrating them into financial management and consumer preferences, fintech businesses hope to increase the usage of digital assistants.

The user's data will be reliably protected by voice biometrics. The owner will be able to buy items, check the balance via voice command, and perform other things at the same time.

44% of people are interested in banking via voice assistants, according to Capgemini Digital Transformation Institute. The Capital One Corporation is a leader in voice payments and has long introduced Amazon Alexa, which enables credit card bill payments for clients.

Other FinTech industry businesses are introducing voice assistants to counsel clients on complicated issues in place of chatbots, managers, and contact centre agents.

Gamification

The application of technology in the financial sector by commercial companies to improve customer experience is known as fintech gamification. Businesses have enhanced revenue, brand loyalty, customer loyalty, and many other beneficial results via gamification. Customers have become more cautious of how companies employ technology as they have become more accustomed to engaging with it.

The gamification market has increased in value over the past five years. Statista reports that spending on gamification increased dramatically from $4.91 billion in 2016 to $11.94 billion in 2022.

Many businesses are implementing gamification into their company strategy to stay interesting and competitive. Companies are embracing gamification like no other. As a result, several businesses have begun utilising games to sell their goods, engage customers, and give them a sense of ownership.

Revolut is a British financial technology company that expanded 45% rise in client base between 2019 and 2020 and attracted 15 million users across 37 countries. Thanks to the gamification strategy, customers of digital banking apps are encouraged to convert to using their Revolut debit card for in-person purchases. Every tenth-time consumers use a card under the Revolut Perks program leads to a reward.

If a consumer uses a Revolut card to make a transaction, cashback rewards will give them a portion of the purchase price back. Discount incentives provide a predetermined discount for traveling or online buying.

Fintech Solution with TechMagic

We have valuable experience developing FinTech solutions from payment automation to personal token creation - from setting integrations to building unique solutions based on B2B fintech trends.

To get a pick of our experience - learn more about how we built the macro-investing app Bamboo. We have a case study with the key points of the project.

If you have a unique idea in mind - do not hesitate to contact us right away. Let’s see what we can do for you to turn ideas into action with trends in fintech 2026.

FAQ

Among many fintech trends in 2026 include the widespread adoption of Embedded Finance, the transformative impact of Open banking, the rise of sustainable finance practices, the continued evolution of Artificial Intelligence (AI), and the dynamic growth of models like "Buy Now Pay Later" and alternative lending, shaping a dynamic and innovative landscape for the fintech industry.

Of course, we do! TechMagic is a fintech software development company that has taken full responsibility for securely recording transactions and tracking assets within a network based on blockchain technology since 2014. Read more about our blockchain development services.

In 2026, the fintech landscape is poised for significant evolution, marked by several key trends. Emphasis on Embedded Finance, where non-financial businesses integrate financial services seamlessly, leads the way. Banking as a Service (BaaS) is gaining traction, fostering collaboration between traditional banks and tech companies. Sustainable finance takes center stage, with a focus on environmentally conscious practices. Artificial Intelligence (AI) and Generative AI continue to shape financial services, offering personalized experiences and innovative solutions. Additionally, "Buy Now Pay Later" and alternative lending models contribute to the dynamic fintech ecosystem.

IThe forecast for the fintech industry is optimistic, indicating sustained growth and innovation. With the rise of Embedded Finance, it's anticipated that more businesses will adopt fintech solutions seamlessly into their operations. Banking as a Service is expected to drive collaborative efforts between traditional banks and fintech startups. Sustainable finance practices will likely become more mainstream as consumers prioritize environmentally conscious financial choices. AI and Generative AI are set to revolutionize customer experiences while emerging models like "Buy Now Pay Later" continue to reshape traditional financial services.

The latest fintech technology encompasses a diverse range of innovations. Embedded Finance is at the forefront, enabling non-financial businesses to offer banking services seamlessly. Banking as a Service (BaaS) transforms emerging markets how financial services are delivered, fostering collaboration and innovation. Sustainable fintech practices incorporate environmental considerations into financial solutions. Artificial Intelligence (AI) and Generative AI are driving personalized customer experiences and enhancing fraud detection. Innovations like "Buy Now Pay Later" and alternative lending models provide flexible and accessible financial services, reflecting the dynamic nature of the evolving fintech landscape in 2026.